Which Trains Stop in Kingston?

A probable station, an unpublished route, and the conditions Kingston City Council actually set.

On 22 July 2026, ALTO chief executive Martin Imbleau told CBC Radio’s Ottawa Morning that Kingston will probably receive a station, citing demand — It’s doable, the ridership is very strong

— because Kingston is a large community. In the same interview he said that most ALTO trains would pass through Kingston without stopping, along with Laval and Trois-Rivières, in order to preserve express service between the larger cities. CBC News

No alignment has been published for the segment that would carry the station. ALTO has said the Montréal–Ottawa route goes to public feedback this autumn, with the Toronto–Ottawa segment — the one containing Kingston — to follow.

The two statements cannot both carry the weight assigned to them. If Kingston’s demand justifies building a station, it justifies serving it; if the timetable cannot absorb the stop, something other than the ridership case is driving the decision. But the more consequential question is not whether Kingston receives a platform. It is how many useful trains Kingston has the day the line opens, counting both operators — and on that question the announcement is silent.

Kingston City Council’s support is not unconditional and never was. Resolution 2026-73, adopted 17 February 2026 by a vote of 9–2, makes support for a southern route contingent upon development along the Highway 401 corridor around the South Frontenac and Kingston region and on a new stop being added in Kingston. It further asks that the route and stop sit as close to the urban core as possible, and resolves that if there is no station in Kingston, council formally opposes the southern route. Of these, the 22 July statement addresses one, provisionally. The 401 contingency and the urban-core request are not addressed at all.

Meanwhile the service Kingston already has is exposed from the other direction. Transport Canada’s 2025–26 estimates record funding to support the planning and eventual transfer of VIA Rail’s Québec City–Windsor corridor operations to the private partner. More than 80 per cent of VIA Rail’s revenue comes from that corridor. A station served by a minority of ALTO trains, combined with a thinned conventional service on the existing line, can leave Kingston with fewer useful daily trains than it has today.

What an intermediate stop costs at 300 km/h

A station call on a high-speed line is expensive in a way that is easy to underestimate. The train must decelerate from line speed, dwell at the platform, and accelerate back to line speed. On comparable systems the round-trip cost of a single intermediate stop is on the order of four to six minutes, before any allowance for the slower alignment geometry often required to reach a city-centre location.

That penalty falls on every through passenger, on every train that stops. Because the project’s commercial proposition is journey time between the anchor cities, the timetable resolves the conflict in the predictable direction: the stop is retained, and most services are routed past it. This is what the chief executive described on 22 July, and it is a rational operating decision given the design speed.

What it does not resolve is the capital exposure. The station, its platforms and approach works, and whatever alignment concession is required to bring the corridor within reach of Kingston are paid for in full, irrespective of how many trains call. A station served by a minority of services carries close to the full cost of one served by all of them while delivering a fraction of the utility. The frequency a passenger actually experiences — not the presence of a platform — determines whether a station changes travel behaviour.

This is not an argument that Kingston should be excluded. It is an argument that a stop and a useful service are different commitments, and that only the first has been signalled.

What Kingston City Council actually resolved

In March 2025, on a motion from the mayor, Kingston City Council voted unanimously to withdraw its support for ALTO. The stated grievance was the change from VIA Rail’s earlier High Frequency Rail proposal, under which Kingston was to have been a regional hub.

On 17 February 2026, council reversed that position. Senior ALTO representatives briefed council that evening, immediately before the vote. Eight delegations spoke to the motion — among them Queen’s University, Kingston Health Sciences Centre, the Downtown Kingston Business Improvement Area, Kingston Accommodation Partners and the Corridor Train Alliance; the minutes record none opposed. A motion to defer consideration to the March meeting was lost 3–8. Resolution 2026-73 then carried as amended, 9–2, with Councillors Glenn and McLaren opposed.

The adopted text is more specific than the public discussion of it has generally been. Its four operative clauses:

Calls on the federal Minister of Transport to enhance ALTO’s mandate to include the addition of a Kingston stop on the proposed ALTO High-Speed Rail Southern Route between Peterborough and Ottawa.

Expresses support for a southern route contingent upon development along the Highway 401 corridor around the South Frontenac and Kingston region, and provided there is a new stop added that is in Kingston.

Requests that the southern route and planned stop be located as close to the urban core of the city as possible.

Resolves that if there is no station in Kingston, council formally opposes the creation of the ALTO southern route as one that would bypass Kingston and offer no benefit to the city or Eastern Ontario.

Clauses 1 and 2 do not describe the same corridor. The first asks the Minister to add a stop to the proposed southern route — the alignment already on the table, which despite its name still passes north of the city, and on which a station would sit roughly 25 to 30 minutes by road from downtown Kingston. The second makes support conditional on a Highway 401 alignment. The 401 contingency entered by amendment (carried 8–3); a second amendment (10–1) softened clause 2’s endorsement of the existing route, and left clause 1 as drafted.

The word “southern” has caused some confusion locally. It describes a route that is southern relative to the Havelock alignment through Peterborough — not one that approaches the lakeshore or the existing rail corridor through Kingston. The practical question for the city is therefore not downtown versus not-downtown. It is whether a Kingston station would be co-located with the existing VIA Rail station, inside the city and inside the existing network, or built new on the far side of it.

That is the inconsistency the two dissenting councillors identified on the night. Their objection was that language open to interpretation would be interpreted by others, and that Kingston risked breaking faith with South Frontenac Township — whose own council had days earlier opposed the line through the township and backed a route through Kingston instead.

Five months later, ALTO can satisfy clause 1 without satisfying clause 2. A probable stop on the existing proposed southern alignment answers the request while leaving the contingency untouched — and nothing said on 22 July distinguishes between them.

| What Resolution 2026-73 conditions support on | What the 22 July statement provides |

|---|---|

| A new stop in Kingston (clauses 1, 2 and 4). Absent one, council formally opposes the southern route. | A station described as probable, three years ahead of the federal decision on whether the project proceeds at all. |

| Status Signalled, not committed | |

| Development along the Highway 401 corridor around the South Frontenac and Kingston region (clause 2) — the express contingency on which support rests. | Not addressed. The Toronto–Ottawa segment is third in ALTO’s publication queue and has not been released for feedback. |

| Status Not addressed | |

| Route and stop as close to the urban core as possible (clause 3). | Not addressed. On the currently proposed southern alignment, which passes north of the city, a station would sit some 25 to 30 minutes by road from downtown and outside the existing rail network. |

| Status Not addressed | |

| Service levels. Not addressed in the resolution, though its recitals rest on Kingston’s established rail demand and on a stop enabling meaningful shifts from passenger vehicles. | Most trains would pass through without stopping. No daily calling frequency has been stated. |

| Status Unstated on both sides | |

The resolution was circulated to the Prime Minister, the Minister of Transport, ALTO’s chief executive, area MPs and MPPs, the Mayor of South Frontenac, and the Eastern Ontario Mayors’ and Wardens’ Caucuses. Its conditions are on the record with every party who would need to honour them.

A new station is a gain only if the service Kingston has survives

Transport Canada’s 2025–26 estimates record funding to VIA Rail to support the planning and eventual transfer of its Québec City–Windsor corridor passenger services to the private partner. That transfer is stated federal intent, not conjecture. More than 80 per cent of VIA Rail’s revenue and more than 90 per cent of its passengers are in that corridor.

The consequence for Kingston follows directly from ALTO’s own numbers. The project’s ridership forecast depends substantially on diverting existing corridor rail passengers — travellers who, by definition, stop buying VIA tickets. The economics of the Kingston Subdivision would then rest on intermediate-point traffic alone, having lost the end-to-end market that carries them. Either frequencies fall, or subsidy rises, or both. This is an observation about the project’s arithmetic, not an accusation about anyone’s intentions.

The commercial logic has already been demonstrated once

In September 2025, VIA Rail announced a pilot running four daily trains non-stop between Montréal and Toronto, bypassing intermediate Eastern Ontario communities. For Kingston it would have removed 33 weekly stops and the first five morning departures, leaving an 11 a.m. first eastbound train and making same-day travel impractical. Kingston, Belleville and Napanee councils passed motions opposing it. It was postponed on operational constraints with CN — not withdrawn — and VIA stated it would continue pursuing direct Montréal–Toronto service.

The same reasoning, ten months later, from the other operator

What ALTO’s chief executive described on 22 July is the same commercial logic, applied to the same city, by operators whose corridor business is slated to converge under the transfer. Kingston’s downside case is not speculative. It was tabled ten months ago, quantified, and shelved rather than abandoned.

The arithmetic Kingston should be doing is net

A platform served by a minority of ALTO services, combined with a thinned conventional service on the existing line, can leave the city with fewer useful trains than it has today — while being announced as a gain. No party is presently negotiating the second half of that equation, and Resolution 2026-73 does not address it.

A long-standing advocate for high-speed rail reaches the same conclusions

On 15 July 2026, Transport Action Canada wrote to the Minister of Transport about the Kingston alignment; the letter was published by the organisation’s Ontario division on 22 July — the same day as the chief executive’s remarks. Transport Action Canada describes a decades-long record of advocating for high-speed rail in this corridor and welcomed the federal commitment to build it. Its letter is not an objection to the project. It is a warning about how this station is being contemplated, and its lead condition is that any ALTO stop in Kingston be co-located with the existing VIA Rail station.

Access time cancels the time saving

Transport Action Canada’s position is that any Kingston station must be co-located with, and fully integrated into, the existing VIA Rail network. Sited instead on ALTO’s currently proposed southern alignment — which they put at approximately 25 to 30 minutes by road from downtown Kingston — it would, in their assessment, likely fail to generate the anticipated ridership and modal shift, because the time spent reaching the station negates the journey-time advantage the line exists to deliver.

The net effect on both operators

The same letter states that such a station would divert passengers from VIA Rail, reducing ridership on existing services and increasing VIA Rail’s operating subsidy requirements — what the organisation calls a lose-lose scenario for both services

. This is the net-frequency problem set out above, reached independently by an organisation that wants the project delivered.

Existing corridors before new right-of-way

The letter closes on the alignment question directly: of the two existing rights-of-way between Montréal and Toronto, one remains largely suitable for high-speed operation while the other could accommodate redirected freight if track capacity were restored. Every opportunity to use existing corridors, it argues, should be explored before undertaking the cost and disruption of an entirely new right-of-way. The letter also notes that the economic rationale and business case for the selected project — including the long-promised Joint Project Office report — have still not been published.

Read alongside Resolution 2026-73, the letter sharpens what Kingston should be asking for. Council’s condition was a station; the more exacting question is which station — one that joins the network the city already uses, or one that starts a second, thinner network beside it.

“We cannot stop in all the communities” is a choice, not a constraint

Asked about a possible stop at Smiths Falls, ALTO’s chief executive said VIA Rail remains an option for smaller communities, and that the project cannot serve every community if it is to remain fast and economical.

The first half of that answer describes a two-tier corridor whose lower tier has no identified funder, no committed frequency, and no infrastructure pathway. The communities on that lower tier — Oshawa, Cobourg, Port Hope, Trenton Junction, Belleville, Napanee, Kingston, Gananoque, Brockville, Cornwall, Dorval — have, with one exception, no viable airport. For most, conventional rail is the only intercity connection to healthcare, post-secondary institutions and economic centres.

The second half is presented as a constraint of physics. It is better understood as a consequence of a design choice. The number of communities a corridor can serve is a function of its design speed: the higher the speed, the more costly each stop becomes in schedule terms, and the fewer stops the business case will tolerate. A 300 km/h line is committed to skipping intermediate cities. A 200 km/h line is not.

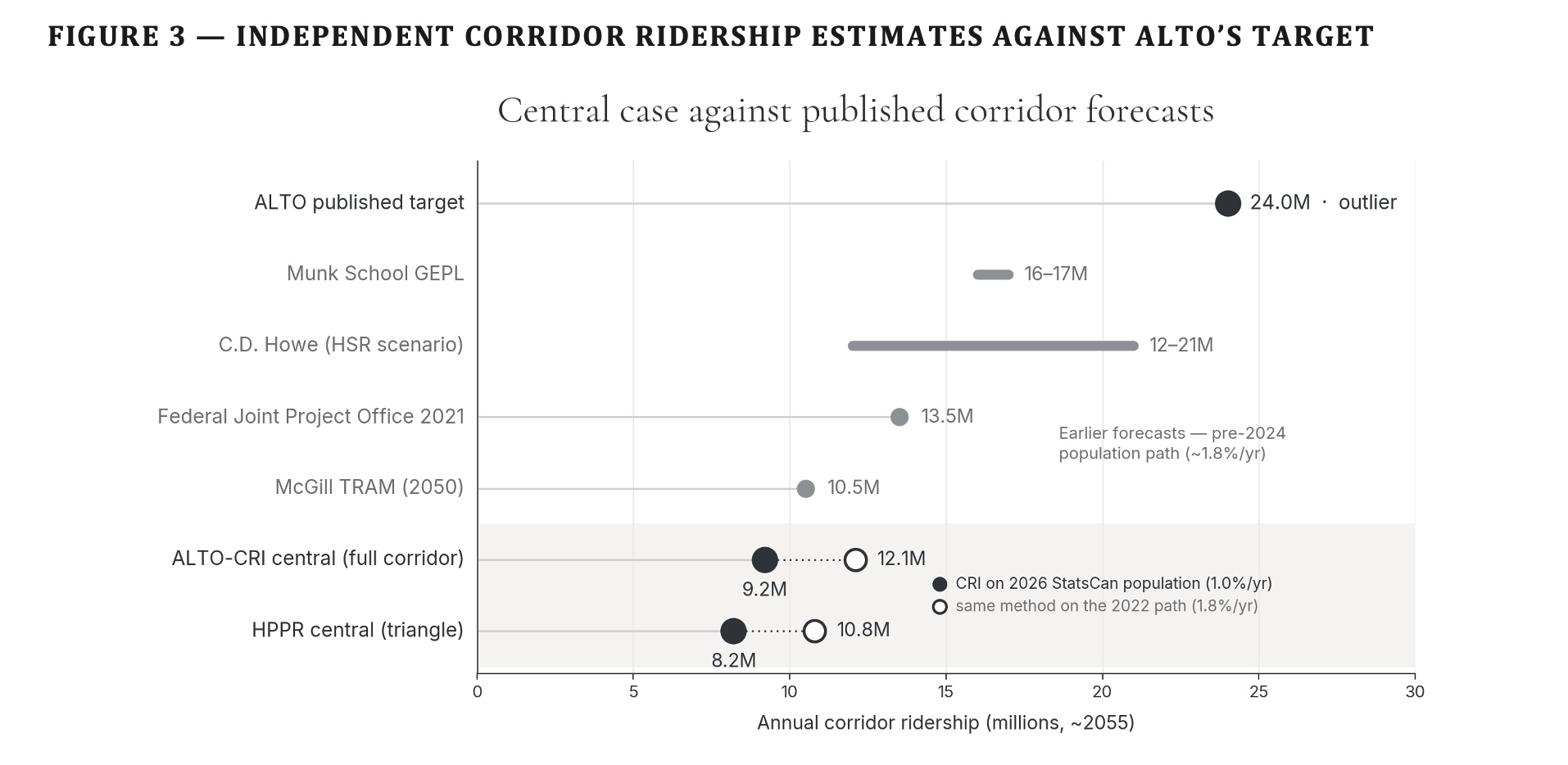

That is the case for High Performance Passenger Rail as an alternative approach — a lower design speed permitting intermediate communities to be served on the fast network itself, rather than skipped and then handed back to a legacy service whose future funding no one has described. It produces a slower headline journey time between Toronto and Montréal, and a materially better network for the roughly one million people living between them.

What could still be settled before the Toronto–Ottawa route is published

ALTO has stated that the Montréal–Ottawa alignment goes to public feedback this autumn, with the Toronto–Ottawa segment to follow. Kingston’s window to convert a signalled station into a specified one closes when that segment is published, not when it is built. The outstanding items divide into two categories.

Within ALTO’s authority to answer now

Requires a federal decision

Summary ledger

Measured against the conditions Kingston City Council itself set:

None of these questions presumes the project fails. Each asks only that the analysis behind the statement be disclosed — and, in the case of the 401 contingency, that a condition Kingston placed on its own support be answered before the Toronto–Ottawa alignment is fixed. Until then, what has been announced is an intention, not a service.