Coalition for Better Rail · Research Brief · The HPR Framework

What is HPR?

An alternative built around the journey people actually take — not the top speed on the brochure.

Chapter 1 · The HPR Framework · Coalition for Better Rail

High-Performance Rail (HPR) is an integrated framework for modernising passenger and freight rail along an existing transportation corridor. Rather than a single greenfield high-speed line, HPR treats the corridor as one system to be optimised as a whole: a new-build passenger spine where new track earns its place, upgrades to existing infrastructure where they deliver more per dollar, and freight capacity improvements that let passenger and freight services each run to their own business model. It is designed to compete on total door-to-door travel time, to reach city centres and the communities in between, and to be delivered in affordable, demonstrable stages.

Download

What is HPR? — Chapter 1 (PDF)

The HPR framework in full: the three-part structure, the ten principles, and the case for a made-in-Canada alternative to greenfield high-speed rail

HPR is not a single thing but a whole-system approach with two working halves. The framework combines a passenger spine and a freight dimension into one corridor strategy, appraised together and delivered incrementally — so each mode can grow to its own business model rather than being forced onto the other’s infrastructure.

HPR — High-Performance Rail · the framework

The whole-system approach. HPR combines the passenger spine and the freight dimension into one corridor strategy, appraised together and delivered incrementally.

HPPR — High-Performance Passenger Rail · the spine

The physical passenger railway: new-build and grade-separated where the corridor requires it, engineered for reliable operation at speeds up to 240 km/h (150 mph), serving downtowns and the communities along the route.

HPFR — High-Performance Freight Rail · the freight dimension

The capacity that untangles freight from passenger obligations. Freed from passenger scheduling, freight can run to a more flexible timetable and operate longer trains — the levers that drive a lower operating ratio — so each mode grows without subordinating the other on shared track.

The Ten Principles

What HPR is built on

01

Holistic optimization. Treat the rail network as a single system to be optimised as a whole, respecting the disparate business models of freight and passenger operations rather than forcing one onto the other’s infrastructure. Avoid projects that monopolize funding, starving the many smaller improvements that would together deliver more.

02

A community railway. Build a railway that benefits the communities along the route, with the potential to deliver genuine, long-term prosperity to the places it passes — integrating them rather than alienating them, and so reducing community friction, political risk and ultimately cost.

03

Untangle freight from passenger. Build the capacity to separate freight from passenger obligations, so each can run to its own service pattern without one subordinating the other.

04

Fast enough. Target typical speeds in the 180–240 km/h band — fast enough to compete door-to-door without the greenfield-only alignments that higher speeds demand. A 240 km/h maximum is also the safer option in extreme temperatures (±30 °C).

05

Safe, comfortable and productive. Deliver a journey a car or plane cannot: grade separation and modern rolling stock make rail among the safest ways to travel, while generous space lets passengers work, rest or connect en route. Time on the train is usable time — a decisive advantage over driving.

06

Frequent and punctual. Compete on turn-up-and-go frequency and dependable punctuality — an on-time performance (OTP) above 90%, sustained through Canadian winters. Reliability, not peak speed, is what earns a traveller’s trust.

07

Downtown access and corridor communities. Prioritise city-centre access and serve the communities along the route, not only the endpoint city-pairs.

08

New-build plus upgrades. Combine new construction with upgrades to existing rail infrastructure, using each where it delivers the most value.

09

Mixed service on shared track. Allow regional, commuter and intercity services to operate over the same tracks, with freed freight capacity as a deliberate co-benefit.

10

Incremental investment strategy. Deliver in stages and invest where benefits are demonstrable — phasing improvements so each tranche earns its place, and avoiding the cost and risk concentration of a single megaproject.

How HPR Differs

A North American solution

The defining difference is what the railway is optimised for. A design that chases 300-plus km/h commits, almost by necessity, to a new greenfield alignment — long straight sections, wide curve radii and bypasses that route around the very communities and city centres a passenger service exists to reach, with speed on the open track bought back in access time, capital and carbon. HPR inverts that priority: by accepting typical speeds in the 180–240 km/h range it can follow the existing corridor, upgrade what already works where prudent, reach downtowns directly, all while liberating capacity for freight — competitive door-to-door at a fraction of the capital exposure, in stages that can be re-scoped as evidence matures.

It is also a difference of provenance. A greenfield high-speed line is essentially an imported experiment — the French passenger-rail model, built for a temperate, densely settled geography and a network that carries no freight. Established North American railroading is the opposite: freight-dominated, shared-track, and tested by hard winters and long distances. HPR is engineered for that reality — made in Canada, for Canadian conditions. It fosters domestic technology transferable to subsequent Canadian projects rather than transplanted from France, and is best understood not as a slower high-speed railway but as a different answer for a distinctly different continent: how to move the most people and freight, to the most useful places, at car-competitive prices, for the most defensible investment with the lowest possible risk.

Travel Time, Not Speed

The clock, not the speedometer

A journey is not a single dash between two stations; it is a chain — reaching the station, waiting for the departure, the run itself, and getting to the final destination at the far end. Top speed touches only one link in that chain. Once access, waiting and egress are counted, the line-haul run is a fraction of the door-to-door total, and shaving it delivers steeply diminishing returns: the gap between 240 and 300 km/h saves minutes on the segment that is already the smallest part of the trip.

Worse, the alignments that permit the highest speeds tend to push stations out of city centres, adding access and egress time that can outweigh whatever the faster run saved — so a train that is quicker on paper can be slower in practice. Frequency compounds the point: a train leaving soon beats a faster one you must wait an hour to board.

The measure that matters

Measured the way travellers actually experience it — and against the car, which over a corridor drive of some 540 kilometres is the real competitor — the figure that matters is the reliable door-to-door clock, not the number on the fastest stretch of track.

The Price Lever

Pricing for a car-centric market

In a car-centric culture, the railway’s real competitor is not the airplane or the existing train but the private car — and against a car already owned, a trip is judged on its perceived marginal cost. That makes price the most direct lever on whether people switch. A line built at megaproject cost must recover that capital somewhere, and fares set to service debt price discretionary travellers straight back into their cars, hollowing out the very ridership the business case assumed. HPR’s lower capital cost is therefore not only a fiscal virtue but a demand strategy: a railway that costs less to build can price to fill trains rather than to service debt. Frequency, downtown access and reliable door-to-door times create the conditions for mode shift; price is what converts them into boardings — and where most trips default to the car, that fare is often the difference between a full train and an empty one.

What HPR Is Not

Neither political, nor all at once

HPR is not a political project. Its route, its staging and its scope follow the evidence — engineering, economics and demographics — not political convenience or partisan preference. Where a claim cannot be grounded in that evidence, it is not made.

Nor is it everything at once. Stage 1 — the scope of the current report — is deliberately bounded: it does not detour via Peterborough, it reaches Ottawa over upgraded existing lines rather than costly new-build, and it defers Québec City to a later stage. Each further stage is added only when the evidence and the need justify it.

The Pitch

A case built to be checked

HPR does not ask to be believed; it asks to be checked. Every figure in its case is meant to be traced to a source, tested against what comparable projects actually cost and carried, and stated with its uncertainty rather than its best case. Where a promotional business case leads with a single confident number, HPR leads with a range and the reference class behind it — because the honest way to forecast a railway is from the record of railways already built, not from the hopes, ambitions and bias of the proponents hoping to build it.

The result is a stronger case, not a softer one. HPR delivers a passenger spine that beats the car on door-to-door time at a fraction of the capital a greenfield high-speed line demands; freight capacity that lifts the operating ratio instead of fighting passengers for slots; benefits that arrive in stages, each proven before the next is committed; and an environmental and cost profile that improves, rather than worsens, once the whole life of the asset is counted. It needs no optimistic ridership and no heroic cost control, and no slick advertorials to stand up. That is the pitch: not the fastest railway that can be drawn, but the one that will be built, used, and pay its way — the case that survives the scrutiny the alternative cannot.

ALTO’s benefits page, set against independent estimates for the corridor — and against the cost figure it never states.

ALTO HSR Citizen Research Initiative · Economic Brief · Published July 2026 · ALTO consultation closed April 24, 2026

⚠ What the page does not say

ALTO’s “Discover Alto’s Many Benefits” page presents at least nine distinct benefit figures — GDP, jobs, tourism, road decongestion, emissions avoided, and annual ridership. It states no capital cost, no operating subsidy, and no benefit-cost ratio anywhere on the page. ALTO benefits page

Every figure on the page is a numerator. The one number that would let a reader judge whether the benefits are worth the spending — the cost of the project — appears nowhere on it.

Critical Finding

The page is built on a single asymmetry: benefits are presented gross, and the cost side is absent. Restore the denominator and the picture inverts. On ALTO’s own official $60–90 billion cost the benefit-cost ratio is only about 0.1; on the Initiative’s higher independent estimate, about 0.06 — against roughly 0.44 for the lower-speed HPPR alternative. Whichever cost figure you use, the benefits recover a dime or less on the dollar, far short of the 1.0 a project needs to break even; the page asks readers to evaluate the project on numerator alone.

On the page’s own headline figures, the ridership claim of up to 24 million passengers by 2055 is roughly 2.6 times the Initiative’s central estimate, and the sustainability claim inverts under full-lifecycle carbon accounting: the Initiative finds ALTO a net emitter of about 15 million tonnes CO₂e over fifty years, while HPPR is a net carbon sink.

This is the standard presentation pattern of optimism bias documented in megaproject appraisal: gross benefits foregrounded, costs and risks kept off the page, and ceiling figures — “up to” — offered as though they were expectations.

The Frame

Benefits gross, cost absent

The GDP line is the clearest instance. The page reports a 1.1 per cent increase in Canada’s GDP, valued at $24.5 billion “in today’s value” — a figure discounted to the present without disclosing the capital sum it is being discounted against. The Initiative’s ECI/CFI cost model puts ALTO at approximately $143 million per kilometre central; over a corridor of roughly one thousand kilometres, the capital envelope is an order of magnitude larger than any single benefit line quoted on the page. The HPPR spine, by contrast, is modelled at roughly $28–40 million per kilometre. ALTO’s own official figure, stated elsewhere, is $60–90 billion for the corridor; the conclusion here does not turn on whose estimate you take, since even on that lower number the benefit-cost ratio is only about 0.1, and on the Initiative’s estimate about 0.06.

Presented this way, the benefits cannot be wrong — only incomplete. A gross benefit is a real quantity; it simply says nothing about whether the project earns it back. That judgement requires the two numbers the page withholds: the cost, and the ridership assumption most of the other benefits depend on.

Comparison

The page’s claims against the corridor’s numbers

Each row sets a figure as ALTO states it beside the corresponding finding from the Initiative’s modelling.

ALTO’s Claim

The Initiative’s Finding

Ridership. Up to 24 million passengers annually by 2055.

The Initiative’s central estimate is approximately 9.2 million in 2055, rising to about 12.5 million by 2080 — roughly 2.6 times lower than the page’s figure. “Up to” marks a ceiling, not an expectation, and the figure coincides exactly with the page’s own 2041 corridor population of 24 million, inviting readers to conflate people in the corridor with trips captured.

Emissions. 100% electric — the equivalent of removing about 100,000 cars from the road each year.

“100% electric” describes operational emissions only. Counted over its full lifecycle — the embodied carbon of a 300+ km/h greenfield build, against a ridership that is itself overstated — the Initiative finds ALTO a net emitter of roughly +15 Mt CO₂e over fifty years. The lower-speed HPPR alternative, built largely on existing alignment, is a net carbon sink.

Economic impact. 1.1% increase in Canada’s GDP ($24.5 billion in today’s value).

A gross benefit stated with no cost and no netting, discounted to present value without disclosing the capital figure behind it. Set against the Initiative’s cost model, the corresponding benefit-cost ratio is approximately 0.06.

Jobs. Over 50,000 during construction; a further 5,000 once operational.

Construction employment is a project input — a cost — not a benefit. Counting it on the benefit ledger is double-counting, among the most reliably flagged errors in megaproject business cases. The 5,000 operational jobs are a genuine recurring effect; the 50,000 construction jobs are not a benefit at all.

Road decongestion. Valued at $570 million.

The figure scales directly off ridership. If the 24 million capture is roughly 2.6 times high, the decongestion benefit is proportionally overstated. Induced demand refilling freed road capacity is not addressed.

Tourism. Approximately $800 million in revenue each year.

A gross figure with no displacement netting — spending that would have occurred anyway, or shifted from elsewhere in the corridor, is not removed.

Travel times. Toronto–Montréal ~3h; Ottawa–Montréal ~1h; Montréal–Québec City ~1h30.

These times are the payoff of the 300+ km/h greenfield alignment that drives both the ~$143M/km cost and the community disruption the page does not mention. HPPR achieves competitive times at 180–240 km/h for a fraction of the cost.

Cost of the project.

Stated nowhere on the page. ALTO’s own official range, given elsewhere, is $60–90 billion; the Initiative’s independent estimate is higher, at roughly $143 million per kilometre. This is the number against which every benefit above would have to be weighed — and the one the benefits page omits.

Three Inversions

Where the page’s strongest claims turn over

The sustainability claim inverts under lifecycle accounting

The page’s environmental case rests on ALTO being “100% electric.” That describes how the trains are powered, not what building the line costs in carbon. A 300+ km/h greenfield corridor — concrete, steel, tunnelling, geofoam, land conversion — carries a large embodied-carbon debt that operational electricity does not offset, particularly once the offset is recomputed against realistic rather than headline ridership. The Initiative’s finding is a net carbon deficit of roughly +15 Mt CO₂e over fifty years, while the lower-speed HPPR alternative is a net sink. The single most quotable line on the page — sustainability — is the one the accounting reverses.

“Up to 24 million” is a ceiling offered as an expectation

The headline ridership number does the persuasive work of the page, and “up to” is doing the work inside it. The Initiative’s central estimate is about 9.2 million passengers in 2055. Systematic overstatement of rail ridership at the appraisal stage is one of the best-documented patterns in the megaproject-forecasting literature, and this figure fits it squarely. The Initiative’s brief The Anatomy of an Optimistic Forecast sets out the mechanism in full.

Construction jobs are counted on the wrong side of the ledger

The page presents “over 50,000 jobs during construction” as a benefit. In a proper appraisal, construction labour is an input the project pays for — part of its cost, not part of its return. Presenting it as a benefit counts the same money twice. This is standard in the appraisal literature, and it is one of the easier errors for a general reader to check.

Three Numbers

What restoring the denominator shows

2.6×

the page’s 2055 ridership claim over the Initiative’s central estimate

Initiative ridership modelling

+15 Mt

net CO₂e over fifty years — ALTO as emitter, not saver, on a lifecycle basis

Initiative lifecycle carbon analysis

0.06–0.1

benefit-cost ratio for ALTO — on the Initiative’s estimate and on ALTO’s own $60–90B; both far below 1.0 (HPPR ~0.44)

Initiative cost & benefit model

None of these three figures appears on ALTO’s benefits page. Each is derived from the page’s own claims once the cost and the ridership assumption are made explicit.

Where things stand · July 2026

Summary ledger

Against the benefit claims as the page presents them:

Overstated

Ridership — “up to 24 million by 2055” is roughly 2.6 times the Initiative’s central estimate of ~9.2 million.

Contradicted

Emissions — the “100% electric” sustainability claim reverses to a net +15 Mt CO₂e deficit once lifecycle carbon is counted.

Omitted

Benefit-cost ratio — no BCR is stated anywhere; the Initiative’s central case is ~0.06.

Omitted

Capital cost — no cost figure appears on the page; central estimate ~$143M/km.

Miscounted

Construction jobs — presented as a benefit; they are a cost input, and counting them double-counts.

Overstated

Decongestion and tourism — gross figures that scale off the overstated ridership, with no netting for displacement or induced demand.

Omitted

Land and community impact — the disruption the 300+ km/h alignment requires is absent from the benefits page entirely.

The page is titled “Discover Alto’s Many Benefits.” The benefits are real as gross figures; what the page withholds is the cost against which they would have to be set, the ridership assumption most of them depend on, and the lifecycle accounting that reverses its environmental claim. Read with those three restored, the case the page makes for the project is substantially weaker than the case it appears to make.

ALTO HSR Citizen Research Initiative, lifecycle carbon analysis — ALTO net +15 Mt CO₂e over fifty years; HPPR net sink.

5.

ALTO HSR Citizen Research Initiative, ECI/CFI cost model (ALTO ~$143M/km central; HPPR spine ~$28–40M/km) and benefit-cost analysis (ALTO ~0.06 on the Initiative’s cost and ~0.1 on ALTO’s own $60–90B; HPPR ~0.44).

6.

ALTO HSR Citizen Research Initiative, “The Anatomy of an Optimistic Forecast” and “A Straighter Line,” citizenresearch.ca.

7.

Bent Flyvbjerg, on optimism bias and reference-class forecasting in the appraisal of major infrastructure projects.

The More You Look, the Worse It Gets — ALTO HSR Citizen Research Initiative

The More You Look, the Worse It Gets

Thirty studies of high-speed rail in this corridor, across fifty-six years. One simple pattern runs through all of them.

ALTO HSR Citizen Research Initiative · A plain-language guide to the record · 2026 · Working synthesis

⚠ The bottom line, up front

The people building the railway say it will pay for itself. The one independent study in 2026 that actually checked the math — using the builders’ own cost estimates — found a hole of about $53 billion over fifty years.

That’s not a fluke. It’s the pattern. For fifty-six years, the case for this railway has looked best in exactly the studies with the most to gain from building it.

In one minute

We read thirty major studies of high-speed rail in this corridor, from 1970 to today, and asked every one the same set of questions — with all the dollar figures put on a level footing.

The verdict almost always matches who paid for the study. Equipment makers, the proponent and paid advocates say build it. Independent governments say wait. And every single study that actually runs the finances finds the same thing: ticket sales can’t cover the cost, so the public pays most of the bill.

The numbers that look great — low costs, huge ridership, big climate wins — come from the promoters. The numbers that survive an independent look are far more sober. The closer and more independent the analysis, the weaker the case.

Read the full report

Corridor Rail Studies, 1970–2026 — A Cross-Decade Analysis

Thirty studies, thirty-four dimensions, nine findings, with the full evidence tables

We didn’t cherry-pick. We took thirty of the major studies of this railway — going right back to a 1970 federal commission — and put the same 34 questions to all of them, so the answers line up side by side across the decades.

30

major studies of this railway, read into one matrix

1970–2026

34

questions asked of every single study

so the answers compare

56

years of studies, all priced in today’s dollars

a level playing field

The studies come from every side: equipment makers, government task forces, a Crown corporation, universities, Transport Canada, and the builders themselves. That range is the whole point — it lets us tell a real change in the corridor apart from a change in who’s doing the asking.

What we found

Nine things every reader should know

Read across all thirty studies, nine patterns keep showing up. Here they are in plain terms.

1The answer depends on who paid for the study

Line up the verdicts and it’s impossible to miss. The build-it studies come from equipment makers, from a Crown corporation that wanted to run the trains, from the proponent, and from paid advocates. Every independent government that looked said wait. Building new is the sponsors’ answer — not what fifty-six years of evidence actually points to.

2It has never paid for itself. Not once.

Every study that runs the money lands in the same spot: fares can’t cover the cost, and taxpayers foot most of the bill. VIA’s own 1984 numbers came out negative. In 1995, three governments agreed the public would cover 70–75%. In 2026, an independent model put the public subsidy at about $53 billion over fifty years — and found the railway wouldn’t even break even until year 44. The promise that it’ll fund itself is the single most optimistic claim in the whole record.

3The closer you look, the more it costs

Whenever a promoter and an independent body price the same thing, the promoter’s number is lower — and the price climbs as the estimate gets more serious. A 2026 advocacy paper gets the cost down to $63 billion only by assuming rock-bottom construction prices, about a third of our own central estimate of roughly $143 million per kilometre. The cheaper the headline, the thinner the math underneath it.

4The ridership numbers don’t hold up

The passenger forecasts are shakier than they look — and academics, an airline, Parliament and Transport Canada have all said so. One 1994 study showed the forecast could swing fivefold just by changing a single modelling choice, on the same data. Transport Canada’s own reviewers called the assumptions “optimistic and aggressive.” And the biggest numbers always belong to the promoters.

5The freight idea is good — with one catch

Splitting passengers and freight onto the corridor’s two parallel tracks, and freeing up freight capacity as a bonus, is a genuinely sound idea — it was proposed back in 2002. The catch: at the time, the freight railways said they didn’t need the extra capacity. It’s a strong argument, as long as it’s honest about that condition.

6Going faster barely helps

Study after study finds that top speed buys almost no extra riders — one found just an 8% jump going all the way from 300 to 400 km/h, another only about 9% from 200 to 300. So the level-headed studies settle far lower: a 2002 plan judged 240 km/h fast enough, and even the independent 2026 model assumes trains averaging just 200–250 km/h. The “top speed everywhere” designs are the outliers — a moderate railway of roughly 180–240 km/h carries nearly the same riders for far less money, and that’s where the evidence actually sits.

7We’ve seen this financing risk before

Having a private partner build and run the railway while the public owns the assets isn’t new — and neither is the warning. Both Parliament (1998) and Transport Canada (2003) flagged the same danger decades ago: deals like this can hand the risk to taxpayers and the reward to investors, with a rosy headline resting on one convenient assumption.

8The climate math only counts the good half

For decades, no study counted carbon at all. Now they do — but only the savings from getting people out of cars and planes. The huge emissions from pouring hundreds of kilometres of concrete and steel and clearing land? Left out. Count both sides honestly and this design adds emissions for decades. That’s the difference between a climate win and a climate cost.

9When the numbers fail, out comes “nation-building”

There’s a move that shows up again and again: when the dollars-and-cents case comes up short, in come national unity, regional growth, and keeping up with other countries. One 2016 report recommended extending the line even at a benefit-cost ratio of 0.24 — about 24 cents of benefit for every dollar spent. These arguments can be fair. But they do the heaviest lifting exactly where the economics are weakest.

The gap, side by side

What the promoters say vs. what independent studies find

All nine findings come down to one contrast. Same railway, same engineering — but the promoters’ numbers and the independent record split apart at every point that matters, and they split the same way every time.

What the promoters say

What independent studies find

Build it new. Equipment makers, a Crown corporation that wanted the contract, the proponent, and paid advocates all say go ahead.

Wait. Every independent government that studied it held off; the reviews and the airlines said upgrade what’s there instead.

The verdict:Build vs Wait

It’ll pay for itself. The 2025 prospectus says the trains will turn a profit — the rosiest claim in fifty-six years.

Taxpayers pay most of it. From 1984 to 2026, every study that runs the money says fares can’t cover the cost. The 2026 independent model: about $53 billion in public subsidy over fifty years.

The money:Self-funding vs ~$53B public

As low as $63 billion. A 2026 paper reaches that number by assuming bargain construction prices.

More like $80–90 billion. The proponent’s own range tops out at $90 billion; independent build-ups land near $80 billion. Costs rise the closer you look.

Price tag:~$63B vs ~$80–90B

24 to 56 million riders. The 2025–2026 figures are the highest ever produced for this line.

About half that. The only recent independent, survey-based forecast lands near 10 million a year — right in line with fifty years of history.

Yearly riders:~24–56M vs ~10M

A big climate win. The proponent headlines a 39-megatonne cut — counting only the savings from fewer car and plane trips.

A climate cost, for decades. The emissions from building it — concrete, steel, cleared land — are left out entirely. Count both sides and it adds emissions.

On carbon:Half the ledger vs The whole ledger

Ridership

Same railway. Forecasts from 6 million to 56 million.

Put the passenger forecasts next to each other and they span almost tenfold — for one railway line. The high numbers always come from the promoters. The one to trust is the recent independent forecast built on an actual survey of travellers.

~10M

independent, survey-based forecast for 2050

McGill, 2026

24–43M

the proponent’s own forecast

ALTO prospectus, 2025

42–56M

the highest numbers ever produced for this line

2026 advocacy paper

Study (year)

Who produced it

Yearly riders

Basis

Air Canada / CP (1993)

Airline / railway

5.8 M

the low end of the record

Task Force (1991)

Governments

7.8 M

full corridor

Tri-government (1995)

Governments

10–12 M

full corridor

EcoTrain (2011)

Governments

10–11 M

full corridor

Lynx (1998)

Private consortium

11.1 M

Québec City–Toronto

SNCF (2010)

Equipment maker

up to 22.5 M

best-case scenario

ALTO prospectus (2025)

Proponent

24–43 M

full network

Advocacy paper (2026)

Paid advocacy

42–56 M

the highest ever

McGill (2026)

Independent

~10 M

survey-based, 2050

The numbers aren’t perfectly apples-to-apples — they cover different routes and years — which is part of the point. The takeaway is simple: the independent, survey-based forecast is about half the proponent’s.

What it means

Five takeaways

The current project sits right at the meeting point of every pattern above. The prospectus is the most upbeat sales pitch in the whole record. The most careful independent 2026 work finds a multi-billion-dollar hole. And the one favourable outside verdict is reached only by pairing the cheapest possible construction cost with the highest ridership ever forecast for the line. Here’s what that adds up to.

What the record points to

Building new from scratch is the sponsors’ pick, not the safe reading of history. Fifty-six years of evidence leans toward upgrading what exists — or waiting for a full, honest costing.

Expect the public to pay most of it. Three governments said 70–75% back in 1995, and every financial study since has landed in the same place.

A moderate-speed, lower-cost railway fits the evidence better. Extra speed barely adds riders, and costs balloon the closer you look. Both have been true for decades.

What to insist on

Get the ridership numbers independently checked before trusting them. A single forecast from the people who want to build it isn’t enough — the best studies in the record always used more than one independent forecaster.

Make the freight case — but be upfront about the catch. The idea is sound; its real value depends on the freight railways actually wanting the freed-up capacity. Say so plainly.

The evidence

All thirty studies, at a glance

Here’s the whole set, oldest to newest. Read the two right-hand columns together — who did the study, and what they concluded — and Finding 1 jumps out: the “build it” verdicts belong to the sellers and the promoters; the governments that were truly independent said wait.

Year

Study — who did it

Independent of the builder?

Verdict

1970

Intercity Passenger Transport Study — CTC

Federal

Upgrade

1984

High-Speed Passenger Rail in Canada — VIA

Crown corp

Mixed

1990

Review of Previous Studies — TRANSURB

Consultant

Wait

1990

A Pragmatic Approach (SPRINTOR) — ABB

Equipment maker

Upgrade

1990

The Canadian TGV Project — Bombardier / GEC Alsthom

Equipment maker

Build new

1991

Rapid Train Task Force — Ontario / Québec

Governments

Wait

1991

Competition in Rail Carriage — Berkowitz

Academic

Build new

1992

FAST TRACKS — VIA (advocacy)

Crown corp

Build new

1993

HST Market Assessment — Air Canada / CP

Airline / railway

Upgrade

1994

Demand-model re-estimate — Gaudry & Le Leyzour

Academic

No verdict

1995

Industrial Strategy (Vol II) — Simpson-Guerin

Consultant

No verdict

1995

Routing & Costing Study — SNC-Lavalin / Delcan

Consultant

No verdict

1995

Québec–Ontario HSR, Final Report — tri-gov

Governments

Wait

1998

The Lynx Proposal — Lynx consortium

Private consortium

Build new

2002

VIAFast — VIA Rail

Crown corp

Upgrade

2003

VIAFast validation — IBI for Transport Canada

Gov’t reviewer

No verdict

2009

Infrastructure and the Economy — Martin Prosperity Inst.

“Advocacy” means a document written to argue a case — a sales prospectus, a think-tank brief, or paid expert advocacy. “No verdict” means the study analysed the question but didn’t take a build/don’t-build position.

The independent studies to trust

Where the sober numbers come from

The full list is above. If you read just a few, read the independent ones — the counterweight to the sales pitch.

1.

Québec–Ontario High Speed Rail Project, Final Report — three governments together, 1995. Concluded the public would cover 70–75% of the cost, and a private-only version couldn’t be financed.

2.

VIAFast validation — IBI Group for Transport Canada, 2003. The government’s own reviewers, who flagged “optimistic and aggressive” ridership assumptions.

3.

Updated Feasibility Study (EcoTrain) — three governments, 2011. The most recent independent-government study; it said wait.

4.

Future of Passenger Rail in Canada — Library of Parliament, 2015. Recommended upgrading service rather than building new.

5.

Corridorwide Survey & Financial Analysis — Transportation Research at McGill, 2026. The independent study behind the $53-billion subsidy figure and the ~10-million ridership forecast.

Build Canada’s case for high-speed rail, measured against the megaproject method the memo itself invokes.

ALTO HSR Citizen Research Initiative · Methodology Brief · Published June 2026 · ALTO consultation closed April 24, 2026

⚠ The Document Under Review

Build Canada’s February 24, 2025 memo, Let’s Show the World How Canada Builds, was published one week after the federal high-speed rail announcement. It endorses high-speed rail in the Toronto–Quebec City corridor and names ALTO directly, while contesting only how the project is delivered — not whether the demand exists or whether the benefit–cost case closes. This brief takes the memo’s argument on its own terms, and holds it to the analytical standard the memo itself sets. Build Canada · original memo

Critical Finding

The memo reaches for exactly the right tools. It quotes Bent Flyvbjerg, the leading scholar of megaproject cost overruns; it calls for reference-class benchmarking against comparable lines; it demands contingency discipline; and it warns that without these, ALTO becomes another HS2 or California High-Speed Rail. On the diagnosis, the Initiative agrees.

The memo then abandons each principle at the moment it matters. It caps contingency at the level that, on its own logic, guarantees overrun. It imports foreign unit costs from a reference class that is not comparable. And it promises true high-speed rail at a unit cost that, in Canadian conditions, only high-performance rail can plausibly reach. Applied honestly, the memo’s own method points away from its conclusion.

The evidence produced since the announcement confirms the diagnosis the memo made and refutes the targets it set. The corridor is still being fundamentally re-routed in the project’s second year; the friction the memo proposed to legislate away has surfaced exactly where the method predicts. The case for caution on ALTO does not require rejecting Build Canada’s framework. It requires applying it.

The Argument’s Shape

What the memo contests, and what it does not

The memo’s argument has a particular structure. It accepts ALTO’s entire benefit case without examination — 40 per cent of the economy, 18 million people connected, up to $35 billion a year in added GDP, travel times halved — and contests only whether the project can be built cheaply and quickly. Every one of those headline figures is the proponent’s own number, repeated approvingly. The memo never asks whether the ridership exists to fill the trains, or whether the benefits exceed the costs.

It asks one question: can Canada build it the way France, Spain, and Japan did? To answer, it reaches for the right instruments — Flyvbjerg’s work on megaproject overruns, reference-class benchmarking, contingency discipline, and the cautionary record of HS2 and California. That choice of tools is what makes the memo worth engaging seriously, and what makes its conclusion fail. The same tools, applied with honest inputs, do not support the case the memo builds on them.

Common Ground

Where the memo is right

Credit first, because the diagnosis is sound. The memo correctly identifies the planning-maturity gap that drives Canadian overruns: our transit projects enter procurement with as little as 1–10 per cent of design complete, where peer countries reach 30–70 per cent. It is right that a strong, technically competent public authority — not a consortium of consultants — must own delivery. It is right that reference-class benchmarking is the antidote to optimism bias. And it is right that HS2 and California are the cautionary tales Canada should study.

None of this is in dispute. What follows is not an argument against the memo’s framework. It is the memo measured against that framework — the standard it asks to be judged by.

Held To Its Own Standard

Three flaws, by the memo’s own method

On three load-bearing claims, the memo prescribes the opposite of what the method it cites requires. The left column states the memo’s own prescription; the right column applies the memo’s own standard to it.

What the memo prescribes

Held to its own standard

1. Cap contingency, including inflation, at 10 per cent. Presented as following global best practice, alongside meticulous benchmarking against French and Japanese lines.

Reference-class forecasting — the very method the memo invokes — requires a larger uplift the less design is complete, because the unknowns are still unpriced. The memo itself concedes Canadian projects sit at 1–10 per cent design maturity. At that maturity, the honest uplift is routinely 40 per cent or more; a 10 per cent cap is defensible only near design completion. The prescription specifies the precise conditions under which budgets break, and calls it discipline.

Verdict:Self-contradictory

2. $25–40M per km; a corridor for under $50B; payback within two years. Drawn from the cost record of France, Spain, and Japan.

A reference class works only if the cases are comparable, and these are not. The cited figures come from older lines, on flatter and cheaper terrain, in earlier cost eras, with no adjustment for what this corridor crosses: the granite of the Canadian Shield, the Frontenac Arch, the wetland and karst of eastern Ontario, and dense urban approaches at both ends. Importing an unadjusted foreign unit cost is exactly the non-analogous-reference-class error Flyvbjerg’s method exists to catch — committed in the section that cites him. The Initiative’s complexity-adjusted estimate runs several times higher, with a central benefit–cost ratio far below the break-even the memo treats as obvious.

Verdict:Wrong reference class

3. True high-speed rail at that same unit cost. Dedicated track, full electrification, grade separation, 300 km/h — delivered for $25–40M per km.

In Canadian conditions, $25–40M per km is not a high-speed-rail figure at all. It is roughly the cost of a high-performance rail upgrade — incremental improvement of existing alignments, the option the memo dismisses in a single line. The memo promises high-speed performance at high-performance-rail prices. The headline product and the headline number belong to two different projects; you cannot buy the performance of one at the price of the other.

Verdict:HSR promise, HPR price

$25–40M

per km — the memo’s claimed unit cost, from France / Spain / Japan

Build Canada memo

≈ $143B

reference-class capital for the corridor delivered as high-speed rail

CRI reference-class analysis

≈ 0.06

central benefit–cost ratio — against the memo’s implied two-year payback

CRI NPV / BCR matrix

“Payback in two years” implies a project that returns many times its capital. The reference-class evidence points to one that returns a small fraction of it. The gap between the memo’s number and the comparable record is not a rounding difference; it is the entire argument.

What Has Happened Since

The diagnosis confirmed, the targets refuted

More than a year on, events have tested the memo’s promises against reality. They vindicate its diagnosis of Canadian megaproject failure and dismantle the targets it set against that diagnosis.

A corridor still being re-routed in year two

The memo set a target of a high-value section carrying passengers within five years, on standardized, locked-in designs, at 10 per cent contingency. Yet the corridor is still being fundamentally re-aligned — a southern-corridor study, a conditional new station at Kingston, an alignment still unchosen between north and south. That is direct evidence of the planning immaturity the memo flagged on its first page — and it makes the memo’s own targets incoherent. You cannot run trains in five years on frozen designs while you are still deciding where the line goes.

Friction exactly where the method predicts

The memo’s prescriptions — sever environmental review from planning, legislate automatic approvals, reduce municipalities to suggesting where infrastructure is placed rather than whether — were aimed at the precise constraints this corridor turns out to be full of: two UNESCO designations, species at risk, organized community opposition, and rural-character concerns that public consultation surfaced in volume. The Initiative’s Community Friction Index has risen from 43 to 54 since consultation began and is projected to climb further. The memo’s answer to friction is not to resolve it but to override it — and on this corridor, that is neither lawful nor likely.

The memo’s own number makes the HPR case

The memo dismisses improving existing rail as insufficient, insisting dedicated high-speed track is the only way. But its own affordability figure, $25–40M per km, is a high-performance-rail number — and the consultation recorded clear public appetite for improving VIA service first and preserving existing Kingston and eastern-Ontario connections. Strip the rhetoric and the memo makes the affordability case for the alternative it rejects.

Conclusion

The antidote that recreates the disease

The memo casts ALTO as Canada’s escape from the HS2 and California failures. Trace its logic, though, and the resemblance runs the other way. “We will build it cheaply and quickly like France and Japan — just cap the contingency and clear the obstacles” is not the cure for optimism bias. It is the textbook expression of it, almost word for word how California began.

The memo’s real service is that it concedes the entire framework. Flyvbjerg, reference classes, contingency discipline, planning maturity: take those tools, feed them honest inputs, and the conclusion does not survive. The case for caution on ALTO does not require rejecting Build Canada’s method — it requires applying it. Done honestly, it points not toward a sprint to high-speed rail at imported prices, but toward a high-performance upgrade of the corridor Canadians actually use, at a cost the country can defend.

Where The Method Lands

Summary ledger

The memo measured against the standard it sets for itself:

Sound

Diagnosis — planning-maturity gap. Correctly identifies that Canadian projects enter procurement at 1–10% design versus 30–70% abroad.

Sound

Delivery authority. Rightly prefers a strong, technically competent public authority over dependence on a consultant consortium.

Sound

Reference-class benchmarking. Rightly names it as the antidote to optimism bias.

Violated

10% contingency cap prescribed at 1–10% design maturity — manufactures the overrun the memo warns against.

Violated

$25–40M/km imported from non-comparable lines without adjustment for terrain, era, or urban approaches.

Violated

HSR promised at HPR price. The headline product and the headline cost belong to two different projects.

Violated

Override of environmental review and municipal consent — aimed squarely at the corridor’s real, documented constraints.

Refuted by events

Five-year passenger target on frozen designs — incompatible with a corridor still being re-routed in the project’s second year.

The memo is at its strongest where it agrees with the Initiative — on method. It is at its weakest where it abandons that method to reach a predetermined answer. Applied honestly, Build Canada’s own framework makes the case for high-performance-rail realism, not for a high-speed sprint at imported prices.

Alto, Public Consultation Report, June 22, 2026 — corridor framing, southern-corridor and Kingston-station feedback, community and environmental concerns.

3.

Bent Flyvbjerg, “What You Should Know About Megaprojects and Why: An Overview,” Project Management Journal (2014) — the megaproject-overrun research the memo cites.

4.

ALTO HSR Citizen Research Initiative — reference-class forecasting, Engineering Complexity Index regression, and de-biased cost analysis for the Toronto–Quebec City corridor.

5.

ALTO HSR Citizen Research Initiative — NPV / benefit–cost matrix and Community Friction Index (post-consultation update).

An ALTO Vice-President says the rail alternative would cost about as much as high-speed rail without the benefits. The government’s own record — and ALTO’s own document — say otherwise.

ALTO HSR Citizen Research Initiative · Analysis · June 2026

In short

In a recent public video, an ALTO Vice-President argues that high-frequency rail would still need dedicated track, would therefore cost about as much as high-speed rail, and would deliver less — a “high cost, low benefit” option. The claim runs against the public record. The government’s own reports costed a dedicated-track high-frequency railway far below high-speed rail, and judged it buildable in a fraction of the time. What shifted that cost to “similar” has never been made public.

On the benefit side, ALTO’s case rests on ridership the international reference class does not support. Tested against ALTO’s own document and the Initiative’s financial analysis, the high-cost option turns out to be the one being built.

The argument is a single chain. High-frequency rail, the video says, is often presented as the cheaper alternative — but it would still require new dedicated track, so its cost would rise to roughly that of high-speed rail, while delivering lower travel-time, ridership, and economic benefits. The conclusion offered to viewers is that high-frequency rail is a “high cost, low benefit” option, while high-speed rail delivers both speed and frequency.

It is a clean story. Two problems sit beneath it before any single figure is examined.

It claims a cost convergence the record contradicts

The video is right that high-frequency rail needs dedicated track — it does not claim trains would share track with freight. Its claim is that building that dedicated track pushes the cost up to roughly high-speed rail’s. The government’s own reports say otherwise, on both cost and time. A dedicated-track, electrified high-frequency railway was costed at $27.7 billion in the December 2021 Business Case — and roughly $4–6 billion in its original 2016 form — and judged buildable in about four years. High-speed rail is now costed at $60–90 billion, on a build horizon stretching into the 2040s. What evidence moved high-frequency rail’s cost and schedule up to “similar” has never been explained, and no side-by-side comparison has been made public.

It never engages the alternative the Initiative proposes

The video treats high-frequency rail as the only alternative to high-speed rail. The Initiative’s proposal is different again: High Performance Rail (HPR) builds dedicated passenger track along existing transportation corridors — such as the CN right-of-way and the Highway 401 — and frees the Kingston Subdivision for freight. It is neither the government’s old high-frequency plan nor ALTO’s high-speed one, and ALTO has never assessed it.

Tested Against the Record

Three claims, three answers

$27.7B

what a dedicated-track high-frequency railway was costed at — against $60–90B for high-speed rail

2021 JPO Business Case

5×

the cost-per-kilometre gap between ALTO and High Performance Rail in the Initiative’s model

$142M vs $28M per km

0.11

ALTO’s central benefit-cost ratio — well below the 1.0 that marks a project that pays its way

Initiative methodology paper

The video makes three factual claims — on cost, on speed, and on benefit. Each can be checked against ALTO’s own published document and the Initiative’s analysis.

The claim in the video

What the record shows

“It would cost on a similar scale to high-speed rail.”

Contradicted by the public record. The government’s own 2021 Business Case put a dedicated-track high-frequency railway at $27.7 billion, against ALTO’s $60–90 billion. Even ALTO’s own Annex B places its “conventional rail” comparator 20–30% below high-speed rail. The Initiative’s reference-class model — a regression across more than forty international projects — puts ALTO at $142M/km and HPR at $28M/km, a five-fold gap. “Similar scale” holds on none of these.

“Without significantly faster travel times.”

Conventional speed already captures most of the benefit. A 177 km/h dedicated-track service was set to cut Toronto–Ottawa from over four hours to about two hours fifty. By ALTO’s own travel-time table, going to 300 km/h saves only a further 17 minutes on Toronto–Ottawa, 19 on Ottawa–Montréal, and 25 on Montréal–Québec. Most of the time saving comes from leaving freight-priority track — not from the extra speed.

“Lower ridership and reduced economic benefits.”

The benefit case rests on ridership the reference class does not support. ALTO’s 24-million-trip target sits outside the achievable modal-shift frontier of 5–12 million annual riders. No operating posture is subsidy-free; each requires roughly $1–3.5 billion per year. The central benefit-cost ratio is about 0.11. The “high benefit” half of the slogan is the half that does not survive checking.

A Note on the Travel Times

Estimated, not simulated

There is a further problem with the speed claim, separate from how small the gain is. The faster journey times were never modelled for this corridor at all. A government record released under the Access to Information Act (file A-2025-00333) shows that the project office produced a detailed RailSys simulation only for the 177 km/h base case. Every faster journey time was a spreadsheet estimate, benchmarked to average speeds on intercity railways in other countries — described in the project’s own memorandum as “for information and comparison purposes” and left to be refined later.

In other words, the under-three-hour trips that make high-speed rail attractive have no corridor-specific engineering behind them in the released record. The one number anyone actually drove through a model of the real line is the slow one.

Read the full record

The Initiative examines this in detail — the two methods, the journey-time tables, and how the speed ceiling was set as a policy target — in a companion research note, Estimated, Not Simulated, based on the same Access to Information release.

The Carbon Case

A carbon debt, not a carbon saving

The video folds environmental benefit into ALTO’s column, on the assumption that faster, higher-ridership rail is the greener choice. The Initiative’s 50-year lifecycle analysis finds the opposite once construction and a decarbonising vehicle fleet are counted. ALTO’s build is a large one-time carbon debt before a single passenger boards — about 14.7 Mt CO₂e in the central construction estimate — and with fifty years of operations the lifecycle total lands at roughly 24 to 27 Mt CO₂e on Ontario’s current grid, and as much as 34 Mt if the grid leans more on gas.

That debt only counts as a saving if the trips it captures would otherwise have been higher-carbon — and the payback math is unforgiving. At the ridership the corridor is most likely to see in its early years, around 4 million passengers a year, no scenario repays the construction debt within a credible horizon. Even at mature ridership, payback runs from a few decades to more than five hundred years, depending on how clean the grid is.

The comparison only worsens with time. By the 2040s, when ALTO might open, much of the car fleet will be electric — and an electric car carrying 1.2 people already emits about 10 g CO₂e per passenger-kilometre, below ALTO’s all-in emissions at every ridership level on today’s grid. Diverting existing VIA Rail passengers, at roughly 25 g/pkm, saves nothing at all. ALTO’s carbon case rests on displacing gasoline cars and short-haul flights — not the fleet that will actually be on the road when it opens.

Most of that debt is greenfield construction. An approach that runs on existing corridors — as High Performance Rail does — avoids the bulk of it, and the single largest carbon lever, shifting freight off congested track, is available whatever the trains’ speed or traction.

Why the Gap Is Real

The cost difference is structural, not arithmetic

The five-fold difference in the Initiative’s model is not an accounting artefact. A 300 km/h design forces a new dedicated greenfield alignment — grade separation, gentle curves, continuous fencing, and large-scale land acquisition — through terrain that scores high on both engineering complexity and community friction. Both the government’s high-frequency plan and the Initiative’s HPR instead run on or alongside existing corridors, which is why each comes in well below the high-speed option. In the Initiative’s model, the gap between high-speed rail and HPR splits roughly evenly between physical engineering and community friction — the cost of the land, the disruption, and the opposition that a new high-speed right-of-way creates.

The Bottom Line

High cost, low benefit — for whom?

The video’s thesis — that high-frequency rail is high cost and low benefit while high-speed rail delivers both — is contradicted by the government’s own record. High-frequency rail was a fully studied, dedicated-track plan, priced at $27.7 billion in 2021 and a fraction of that in its original form, and due to be carrying passengers now. The decision to replace it with a 300 km/h, $60–90-billion project was taken without a published comparison; the video supplies the missing conclusion after the fact.

On the evidence available, the high-cost option is the one that was chosen. The lower-cost alternatives — the government’s own, and the Initiative’s — were set aside without being weighed in public. That is the question the slogan invites, turned back on itself: high cost, low benefit, for whom?

Sources

Primary documents

1.

ALTO, Fast Forward: Shaping Canada’s Future with a High-Speed Rail Network (March 2025) — cost ranges, travel times, and ridership targets, main text and Annex B. altotrain.ca

2.

Joint Project Office High Frequency Rail Project, Business Case Update, V.002 (December 10, 2021) — dedicated-track design, $27.7 billion costing, and four-year construction estimate.

3.

The Globe and Mail, “Transport Canada reviewing studies on Via Rail expansion” (July 2017) — the original 2016 high-frequency concept at roughly $4–6 billion. theglobeandmail.com

4.

“VIA HFR-TGF Journey Times” memorandum and accompanying email chain (August–September 2023), released under the Access to Information Act as file A-2025-00333 — simulated base case versus estimated higher-speed times.

5.

ALTO HSR Citizen Research Initiative, ALTO Financial Analysis (methodology paper and supporting research notes) — cost-per-kilometre model, ridership frontier, subsidy spectrum, benefit-cost ratio, and lifecycle carbon. ALTO-Financial-Analysis.pdf

6.

ALTO HSR Citizen Research Initiative, 50-Year Lifecycle CO₂ Budget — Parametric Analysis (March 2026) — construction, operational, payback, and modal-comparison figures, drawing on HS2, UIC, and international HSR lifecycle studies.

7.

Statements examined: public video by an ALTO Vice-President (June 2026).

A plain-language guide to how we evaluated the cost of the proposed ALTO high-speed rail line — starting from one simple rule that every railway in the world has to obey, and following it through to a number the government’s own claims do not match.

ALTO HSR Citizen Research Initiative · Financial Framework · Published May 2026

⚠ What this is

This is the readable version of a longer technical paper. The full document and slide deck show every calculation; this post explains, in everyday terms, what we did, why, and what we found — with no maths background assumed.

The short version: the project’s likely capital cost is roughly double what the government has stated; the trains cannot pay for themselves at any realistic ticket price; and the project’s headline ridership target of 24 million passengers a year sits outside the range that any comparable line has ever achieved.

The one idea to take away

Every operating railway in the world has a bill that has to balance every year. What it costs to build and run the line on one side; where the money to cover that comes from on the other. The money can only come from three places: ticket sales, a government subsidy, or value captured from land near the stations.

You can argue about any single number. What you cannot do is leave one side of the bill short. If a proponent quotes you a low cost and a high number of riders but never tells you the subsidy, the subsidy is simply the part of the bill they haven’t shown you — it doesn’t disappear. Our whole method is just: fill in every blank on the bill using independent evidence, and see what the missing number turns out to be.

Read in full

A Framework for Independent Evaluation of the ALTO HSR Project

The complete methodology, every rubric and dataset, and a slide deck version — all published and reproducible

Imagine your household budget. Whatever you spend has to be matched by money coming in — from your salary, your savings, a loan. A railway is no different, just bigger. There are two kinds of cost: the enormous one-time cost of building the line (paid off gradually, like a mortgage), and the ongoing cost of running it every year — staff, electricity, maintenance, replacing worn-out trains.

Those costs have to be paid for. There are only three sources. Here is the whole thing on one line:

The annual fiscal ledger

Cost to build (yearly share) + cost to run=ticket sales + government subsidy + land value capture

The left side is what the railway costs each year. The right side is where that money comes from. The two sides must be equal — that’s what “balance” means.

In plain terms

“Land value capture” means a railway can sometimes raise money from the rise in nearby land prices that a new station creates — for example by developing land around the station. It’s a real tool, but a modest one in Canada, and ALTO has named no such mechanism. So for ALTO that third source is effectively zero, which leaves only two: tickets and subsidy.

Here is the consequence that does all the work. Once you’ve pinned down the cost, the ticket revenue, and the land capture using evidence, the subsidy isn’t a choice anyone gets to make — it’s whatever is left over to make the bill balance. It’s a leftover, not a decision. That single insight is why a project can claim to be “self-sustaining” and still, on its own numbers, need billions of dollars of public money a year. The subsidy was always there; it just wasn’t written down.

The Method

Seven steps to fill in the blanks

To fill in each part of that bill honestly, we built a seven-step process. Each step answers one question using published evidence rather than the project’s own marketing, and each step shows its work so that anyone who disagrees can re-run it with their own assumptions. Here is what each step asked, and what it found for ALTO.

1

How hard is this to build?

Engineering complexity, compared to rail lines around the world

We scored the corridor’s technical difficulty against an international database of comparable projects. ALTO lands in the upper “High” band — among the most demanding corridors anywhere in the world. Hard things cost more and run late more often; this matters for every number that follows.

2

How smooth will getting it approved and built be?

Community, consultation and consent risk

We measured the friction the project faces from communities, landowners and the consultation process. The score lands in the band where comparable megaprojects’ cost overruns tend to cluster — another reason to expect the final bill to climb.

3

What will it really cost to build?

Capital cost, calibrated against similar projects

The government states $75 billion. Comparing ALTO to a reference class of similar railways and adjusting for its difficulty, our central estimate is $143 billion — nearly double — with a worst-case ceiling of $264 billion. The stated budget sits at the very bottom of the plausible range.

4

What will it cost to run, every year?

Operating cost, built up from the actual assets

Adding up staff, operations, maintenance and replacing trains as they wear out gives about $2.15 billion a year. To cover just that running cost from fares, the line would need roughly 12.5 million passengers a year — and even then it only recovers about 80 cents of every dollar.

5

How many people would actually ride it?

Realistic ridership, and the subsidy that follows

Based on how many travellers comparable lines actually pull off the roads and out of the air, a realistic range is 5 to 12 million riders a year, with a sensible target near 8 million. ALTO’s headline figure of 24 million sits outside that range entirely.

6

Is it worth it?

Benefits weighed against costs

Weighing all the benefits against all the costs gives a ratio of about 0.11 — roughly eleven cents of benefit for every dollar spent. To make the 24-million target pay, tickets would need to cost between $381 and $1,596 — and 24 million riders is unreachable anyway.

7

Would a serious gatekeeper approve it?

Tested against Norway’s independent project-review system

Norway runs big projects through two independent quality gates before funding. Run through those gates, ALTO fails most of the criteria at both stages — described as a textbook example of exactly the kind of project the Norwegian system was built to catch.

What “reference class” means

Rather than trust a project’s own optimistic forecast, you line it up against a large group of similar projects that have already been built, and ask: what actually happened to those? It is one of the most reliable ways known to forecast cost and ridership, precisely because it sidesteps wishful thinking.

The Headline Figures

Three numbers that frame the whole thing

Cost to build

$143B

Our central estimate — against a stated budget of $75B

Value for money

11¢

Of benefit returned per dollar spent (a benefit-cost ratio of 0.11)

Ridership gap

24M

The stated target — against a realistic ceiling near 12M

None of these is a guess plucked from the air. Each one is the output of one of the seven steps above, and each step publishes the data and the scoring behind it. The point of putting them together is simple: a project whose costs are understated, whose value-for-money is low, and whose ridership is overstated does not become viable just because its three weaknesses are described in separate documents.

The Part Nobody Mentions

No ticket price makes the bill disappear

Here is where the “bill that has to balance” idea pays off. There is a temptation to think the subsidy could be designed away — charge higher fares, or fill more seats. So we tested the three obvious strategies. In every case, a large public subsidy remains. The only thing that changes is how the cost is split between the passenger and the taxpayer.

Charge premium fares

~$1B / yr

Trade-off:High ticket prices, so fewer riders. Lowest subsidy — but still about a billion a year.

Match airline fares

~$2B / yr

Trade-off:Prices in line with flying. A moderate middle path — roughly two billion a year.

Deep discounts, fill seats

~$3.5B / yr

Trade-off:Cheap tickets, more riders — but the lowest fares mean the largest subsidy.

Notice what this means. Choosing among these isn’t a choice between “subsidised” and “unsubsidised” — every option is subsidised. It’s only a choice about who pays: the rider at the ticket window, or the taxpayer through the public purse. That is a perfectly legitimate political decision to make out in the open. What isn’t legitimate is pretending the choice doesn’t exist.

And that is exactly why one specific government claim does not hold up. On 22 April 2026, the government stated the operation would be “financially self-sustaining” — meaning fares alone would cover running costs. But no realistic level of ridership produces enough ticket money to cover the $2.15 billion annual running cost. Measured against every comparable high-speed line operating in the world, that claim simply isn’t consistent with the evidence.

The Bottom Line

What the filled-in bill shows

Put the seven steps together and the picture is consistent, not cherry-picked:

Roughly double the cost

The likely cost to build is about twice the stated budget — and the stated figure sits at the bottom edge of what’s plausible.

Cannot pay its own way

At no realistic fare do ticket sales cover even the cost of running the trains, let alone building the line.

Eleven cents on the dollar

The central value-for-money ratio is about 0.11 — far below the level at which a project is normally considered worthwhile.

A ridership target out of reach

The 24-million figure lies outside the range any comparable line has achieved, and the subsidy is required no matter what.

Measured against Norway’s independent review standard — one of the most respected gatekeeping systems for large public projects — ALTO fails the majority of the tests at both the early-concept stage and the pre-funding stage.

In Fairness

This is a recommendation, not a verdict

It matters how this is meant to be read. The seven-step process produces a recommendation, not a decision. The decision belongs to elected officials and the public — ideally informed by an independent authority such as the Parliamentary Budget Officer.

The purpose of all this work is narrow and, we hope, fair: to put a balanced, contestable record on the table, so that the choice about which rail corridor Canada builds rests on evidence rather than on headline numbers. Every step publishes its rubric, its scoring, and its data. If you disagree with any finding, you are invited to re-run it under your own assumptions — that openness is the whole point.

A good public investment can survive this kind of scrutiny. The questions below are the ones any major rail proposal should be able to answer plainly.

On cost: If the stated budget sits at the bottom of the plausible range, what is the realistic central figure — and what happens to the case if the cost lands there?

On the subsidy: Since fares cannot cover running costs at any realistic ridership, what annual public subsidy is the government planning for, and who decided how to split the cost between riders and taxpayers?

On ridership: What evidence supports 24 million riders a year when comparable lines top out far below that — and what does the business case look like at a realistic 8 to 12 million?

None of these questions presupposes opposition to passenger rail, which many people support. Each asks only that the project state plainly what its own numbers imply — so the public can weigh a real proposal rather than a hopeful one.

Read the full framework

A Framework for Independent Evaluation of the ALTO HSR Project

The complete methodology, the seven-stage pipeline, and every rubric, score and dataset — published and reproducible

Citizen Research Initiative · Financial Analysis · NPV Note 1

NPV and BCR Projections for ALTO

A deterministic net-present-value analysis over 2029–2080 across three capital-cost scenarios, three operating regimes, and four discount rates — thirty-six combinations, every one of them strongly negative.

ALTO HSR Citizen Research Initiative · NPV Note 1 · Net Present Value Analysis 2029–2080 · Published May 2026 · updated June 2026

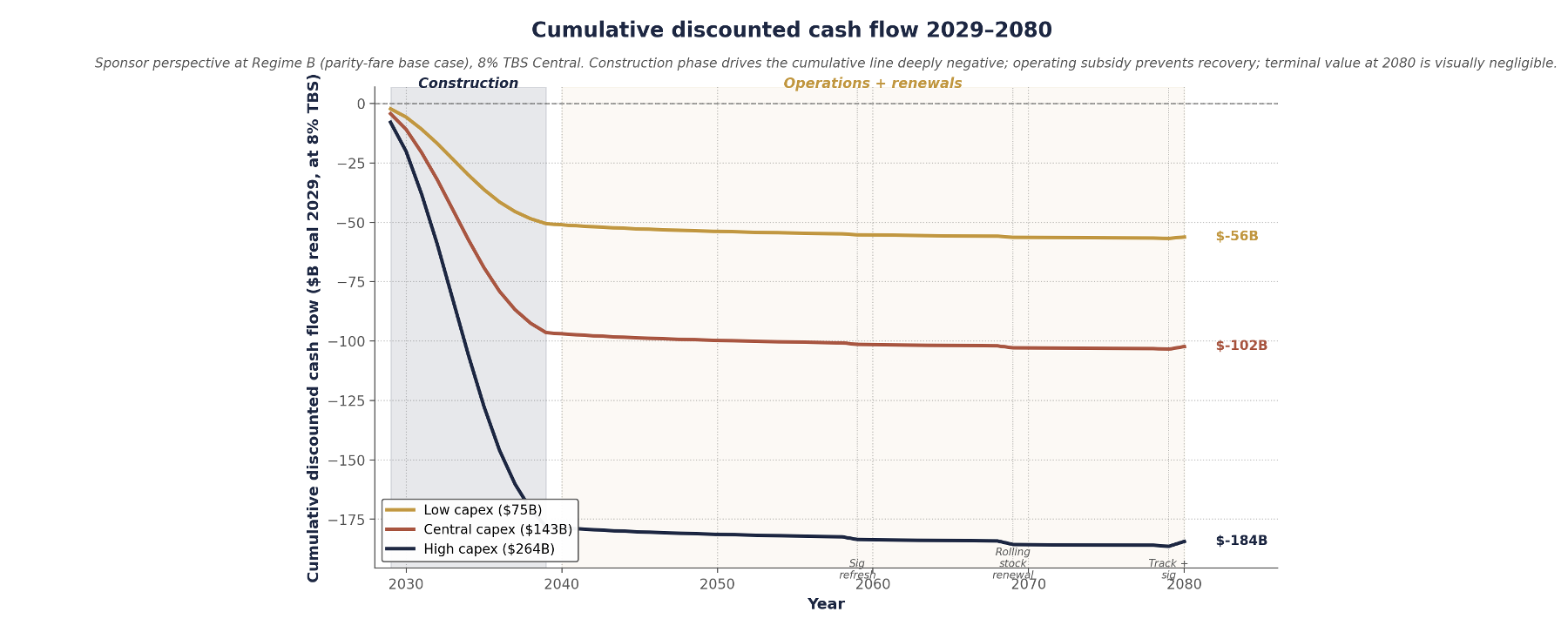

⚠ Headline Finding

Across 36 combinations of capital-cost scenario, operating regime, and discount rate, ALTO produces a financial NPV between −$50 billion and −$246 billion in real 2029 CAD. At the Treasury Board central 8% rate and the welfare-efficient Regime B posture, NPV is −$56B at $75B capex, −$102B at $143B, and −$184B at $264B.

The benefit-cost ratio across the 9-cell capex×regime grid runs from 0.030 to 0.107 — every cell at least nine times below the 1.0 break-even threshold. Capital cost is the dominant driver; operating regime is second-order; the discount rate changes magnitudes but not the direction.

Executive Summary

This report evaluates financial and combined NPV over a 52-year horizon, integrating the engineering operating-cost build of the Cost-of-Running-the-Train work with the modal-shift subsidy frontier — a coupled analysis in which ridership, fare, operating cost, and operating subsidy are determined jointly along the corridor’s achievable frontier.

Three capital-cost scenarios bracket the plausible range: a low case at ALTO’s published $75B (~P2.5 of the reference class), a central case at $143B (the reference-class mean under Flyvbjerg’s overrun distribution), and a high case at $264B (the P97.5). Three operating regimes from the subsidy frontier set the achievable operating points: premium (Regime C, 6.1M pax), parity-with-air (Regime B, 8.2M, the revenue peak), and deep-discount (Regime A, 11.2M, near the modal-shift ceiling).

Cost-recovery break-even from fares alone sits at 117 trains/day, or 12.5 million annual passengers at the reference yield — above the modal-shift ceiling. All three regimes operate below it and require ongoing federal operating subsidy. The PV of that subsidy stream is structurally independent of capital cost ($4.6B at Regime C to $7.6B at Regime A at 8%). And the 24-million-by-2055 figure in ALTO’s public materials sits outside every operating point on the frontier and is not modellable under any defensible parameter combination.

Download

NPV Note 1 — NPV and BCR Projections for ALTO (PDF)

The full report with all six figures and nine tables: the three capital scenarios, the three operating regimes, the four discount-rate NPV tables, the operating-subsidy stream, the economic overlay, the benefit-cost grid, and the methodology and parameter appendices

This report presents an NPV analysis of ALTO over 2029–2080, in real 2029 Canadian dollars from the project-sponsor perspective, with a parallel economic overlay for passenger and external benefits. The objective is a defensible quantitative basis for evaluating the project against the standard Treasury Board cost-benefit framework.

The framework integrates two pieces of prior work. Annual operating cost is built from the lifecycle methodology of the operating-cost note — infrastructure maintenance, train operations, and fleet recapitalisation. Ridership, fare, and operating subsidy are determined jointly by the three operating regimes of the subsidy-frontier note, which establish the achievable points on the corridor’s modal-shift frontier. Capital cost is treated through reference-class forecasting, with three scenarios spanning the empirical distribution of cost outturns on comparable HSR megaprojects. Operations are assumed to commence in 2040 after an eleven-year construction period; cash flows include capex during construction, operating cost and ramped fare revenue, three lump-sum renewals at operating years 20/30/40, and a terminal residual at 2080.

−$102B

Financial NPV, base case ($143B capex × Regime B × 8%)

0.030–0.107

Benefit-cost ratio across the 9-cell grid — all ≥9× below break-even

~94%

Share of the negative present value driven by capital cost alone

2 · Capital Cost

Three scenarios from the reference class

Capital cost is the largest single quantity in the analysis and the dominant source of NPV uncertainty. Three scenarios span the plausible range, calibrated by reference-class forecasting on the international HSR cost database (log-normal, mulog = 4.963, sigmalog = 0.312).

Low — $75B

ALTO’s published figure (the centre of the $60–90B Fast Forward range). Sits at ~P2.5 of the reference class — a lower-tail estimate consistent with megaproject optimism bias. Predates the HFR→HSR scope expansion and carries no published contingency.

Central — $143B

The reference-class mean. Applying Flyvbjerg’s 44.7% average rail overrun to the baseline, plus ALTO’s engineering-complexity premium (composite 73–81), gives the modal outcome — the appropriate base case for procurement decisions.

High — $264B

The P97.5 — exceeded by ~1 HSR project in 40. Not a theoretical bound: HS2 Phase 1 (~+250%), California HSR (~+200%), and HSL-Zuid (228%) all approached it. The corridor’s geology and the Canadian P3 record make it a realistic case.

The three scenarios are not equally probable: under the calibrated distribution, the proponent’s figure has roughly a 2.5% chance of being achieved or undercut, the central scenario is the modal outcome, and the high scenario reflects upper-tail risk. Treating $75B as the planning case would require ALTO to be delivered with cost discipline materially better than every comparable international HSR megaproject — a claim for which no evidence has been adduced.

3 · Operating Regimes

Three points on the achievable frontier

The three operating regimes derive from the subsidy frontier. Each is an internally consistent point on the corridor’s achievable modal-shift frontier, with ridership, fare, revenue, and subsidy following from a single fare posture. No operating point produces high ridership at low subsidy.

Table 2. Operating regime parameters (central 2055 demographic anchor). Operating subsidy = max(0, operating cost − fare revenue). Mature values shown; in operating years 2040–2047 ridership and revenue ramp from 50% to 100% of mature values.

Parameter

Regime C — premium

Regime B — parity

Regime A — discount

Rail-to-air fare ratio

1.4

1.0

0.55

Average fare ($/trip)

$207

$157

$96

Mature ridership (M pax/yr)

6.1

8.2

11.2

Modal share captured

22%

30%

40%

Annual fare revenue ($M)

$1,260

$1,290

$1,080

Annual operating cost ($M)

$1,928

$2,116

$2,385

Annual operating subsidy ($M)

$668

$826

$1,305

Regime B is the welfare-efficient point under standard cost-benefit assumptions — simultaneously the revenue-maximising point and the per-rider welfare-efficient point. A profit-maximising private operator and a welfare-maximising public authority applying marginal analysis would converge on it, even if they would disagree on whether to operate the corridor at all. Regime A, at 11.2M, approaches the modal-shift ceiling of ~12M; pushing beyond would require corridor-external policy (highway tolls, fuel pricing, aviation limits). The 24-million figure sits above the ceiling — reaching it would require doubling modal share to ~80%, far below cost recovery, and is not modellable as a financial NPV.