ALTO Ridership Against the Modal-Shift Evidence

What the published 24-million target implies for how many travellers must abandon air and car for the train — and what the modal-shift evidence, the demographic baseline, and the operating-subsidy frontier say is actually reachable on the corridor.

This brief draws together four CRI research notes — on rail–air substitution (Note 1), rail–car substitution (Note 2), the ALTO ridership envelope (Note 3), and the operating-subsidy frontier (Note 4) — into a single test of one number: ALTO’s published target of 24 million annual passengers by 2055.

Each note is built from the same starting point as the proponent’s own forecasts, but corrected for two things older studies omit: the North-American calibration of modal-shift behaviour, and the 2024 federal cap on non-permanent residents that broke the corridor’s demographic trajectory.

ALTO’s published target of 24 million annual passengers by 2055 sits 2.6× above the CRI central case of 9.2 million, and is incompatible with every other independent forecast for the corridor.

The gap is not a matter of optimism versus pessimism. Reaching 24M requires a modal share above the ceiling the modal-shift curves allow in a North-American setting; it assumes a population trajectory the federal government’s own immigration policy has already foreclosed; and pushing ridership toward the target through deeply discounted fares drives operating subsidy past $5 billion a year. The target fails three independent feasibility tests at once.

- Note 1 Modal shift between high-speed rail and air — the rail–air S-curve and the competitive zone

- Note 2 Modal shift between rail and car — the North-American–calibrated rail–car curve and the group-size effect

- Note 3 The ALTO ridership envelope — population × trips × modal share, scaled by phasing, vs the 24M target

- Note 4 The operating-subsidy frontier — the trilemma of ridership, subsidy and P3 break-even, and why 24M sits off the frontier

How many people would actually have to switch?

A ridership target is, underneath, a claim about behaviour. To carry 24 million passengers a year, the corridor must persuade a very large share of the people now flying or driving between Toronto, Ottawa, Montreal and Quebec City to take the train instead. That share — the modal shift — is the quantity every forecast turns on, and it is the quantity this brief examines first.

Modal shift is not a free parameter. Decades of evidence from operating high-speed lines show it follows a predictable shape: rail captures most of the market on short, fast journeys and loses it on long ones, with a sharp transition in between. The question for ALTO is not whether modal shift happens — it plainly does — but how high the curve can realistically reach on this corridor, in this country, at the fares the project would have to charge.

Three forces set that ceiling: the journey-time geometry against air, the harder competition against the car in a North-American setting, and the price the traveller actually faces. The notes treat each in turn before combining them into a ridership envelope and testing the 24-million figure against it.

Modal shift versus air follows a logistic S-curve

Against air, rail’s market share is governed almost entirely by station-to-station journey time. The relationship is a logistic S-curve: below about two hours rail dominates, between two and four hours the two modes compete and infrastructure quality is decisive, and beyond about five hours rail share collapses to only the price-sensitive or rail-loyal traveller. The inflection point — where rail and air split the market evenly — sits at roughly 3.5 hours.

This is not theory. The world’s operating high-speed lines trace the same curve, and they are the empirical anchors the note is calibrated against:

- Paris–Lyon (TGV): rail share rose from 40% to 72% after high-speed service opened.

- Madrid–Barcelona (AVE): roughly 75% rail share at a 2 h 30 min journey time.

- Madrid–Seville: rail share rose from 16% to 52%.

- Beijing–Shanghai: 1,318 km covered in 4 h 18 min, rail-dominant despite the distance.

For ALTO, the implication is straightforward: the air-substitution share the corridor can win is bounded by where each city-pair sits on this curve. Pairs that fall inside the two-to-four-hour competitive zone can deliver strong rail capture; pairs that fall outside it cannot, regardless of how the target is set.

Modal shift versus the car is harder in North America

The car is the larger and more stubborn competitor, and here the North-American context shifts the whole curve against rail. The note re-calibrates the rail-vs-car S-curve on VIA Rail’s observed performance — a rail share of roughly 13% against road — and finds the inflection point moves sharply left: from τ = 0.65 in the European setting to τ = 0.46 in the North-American one, a 19-point shift.

Why North America shifts the curve

Toll-free highways run the 401/A20 corridor end to end. Fuel taxes are roughly one-third of European levels. There is no congestion charging anywhere in Canada. And family-car economics are decisive: per-person car cost divides among the occupants, while rail charges per ticket.

What this does to predicted share

The same corridor that would capture a healthy rail share in Europe captures materially less here. The gap between the European and North-American readings is the single largest correction separating the CRI work from the older forecasts.

Carried through to the ALTO city-pairs, the North-American calibration produces predicted rail shares of the rail+car market that sit well below the European equivalents:

- ALTO Toronto–Ottawa (τ ≈ 0.44): about 51% North-American versus 67% European.

- ALTO Toronto–Montreal (τ ≈ 0.56): about 41% North-American versus 58% European.

- HPR on both pairs (τ ≈ 0.65–0.67): about 33% North-American versus 50% European.

The lesson is that a forecast borrowed from European experience — as the older studies effectively are — systematically overstates how much of the road market the corridor can win. The car does not behave here the way it behaves there.

Price shifts the whole modal-shift curve

Journey time fixes the shape of the S-curve; price selects which curve in the family the corridor actually sits on. The relevant variable is the fare-to-comparator price ratio (r) — rail’s price relative to the air fare or the per-person car cost it competes with. A lower ratio lifts the entire curve; a higher ratio depresses it.

Elasticity differs by mode

Road–rail substitution is more price-sensitive than air–rail (γ = 1.5 versus 1.0). Travellers deciding between train and car respond more sharply to fare changes than those choosing between train and plane.

Group travel hurts rail

Per-person car cost divides among the occupants; rail charges per ticket. A family of four therefore faces an effective price ratio roughly four times higher than a solo traveller — pushing them down the curve toward the car.

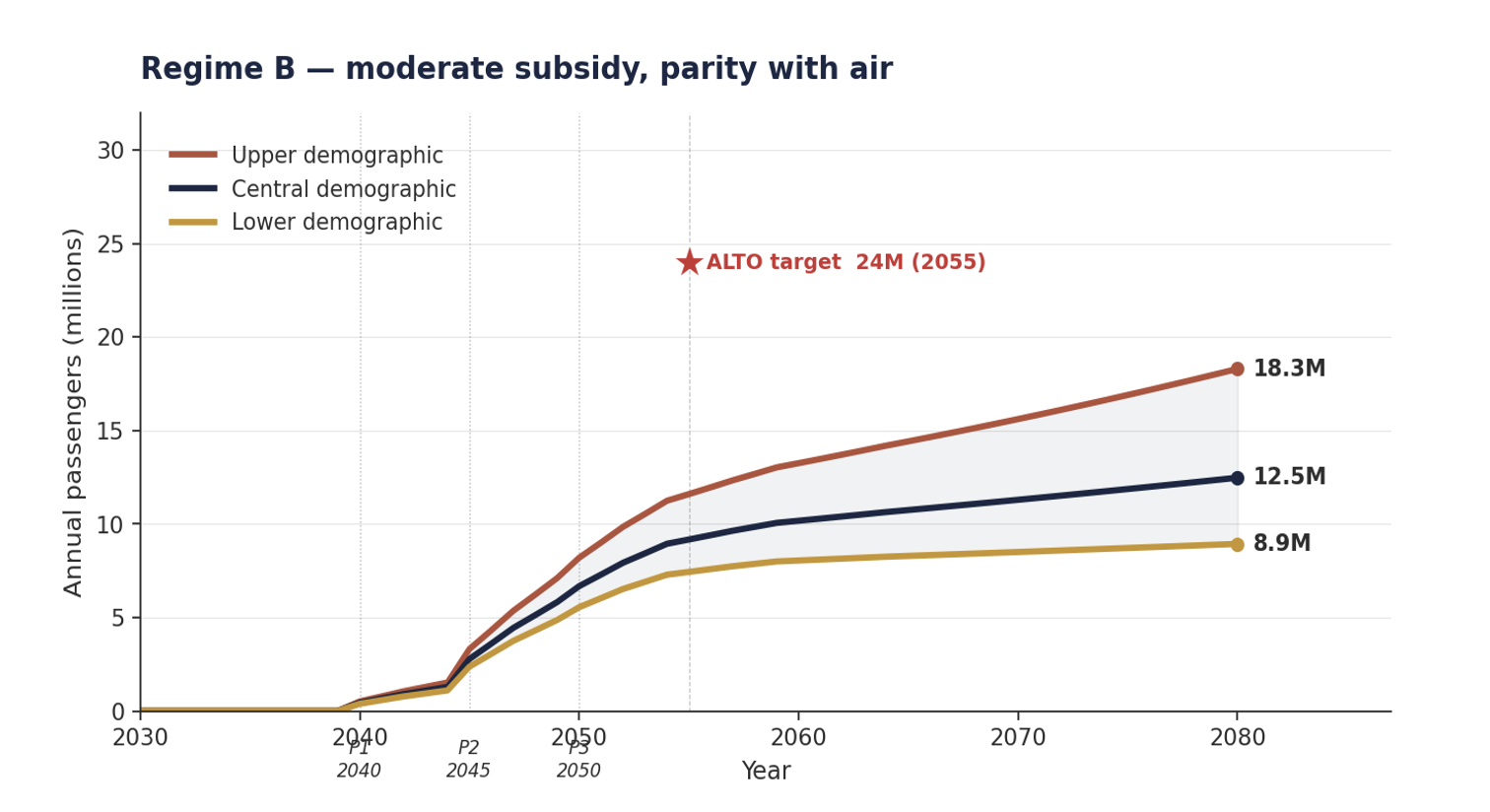

The note maps three fare regimes onto the curve family. Regime A (r ≈ 0.55) is deeply discounted, lifting share but requiring heavy subsidy. Regime B (r ≈ 1.0) sets fares at parity with air. Regime C (r ≈ 1.4) prices above the comparator. Each selects a different curve — and, as Note 4 shows, a different point on the subsidy frontier. The crucial consequence is that the high-share outcomes the 24-million target needs are only available at the discounted end, where the fares no longer cover the cost of carrying the passenger.

The 2055 envelope is 3.7 to 17.2 million

Combining the modal-shift ceiling with the corridor’s demographics produces a ridership envelope, not a single number. The framework is deliberately transparent: ridership = population × per-capita trips × modal share × ramp-up. Each input is drawn from published data and stated openly.

The demographic inputs are post-2024 and this is where the CRI analysis departs most sharply from the others. The corridor population is 14.9 million (2025), residents make about 1.68 intercity trips each, and StatCan’s low / medium / high growth scenarios run at 0.5% / 1.0% / 1.6% per year. Critically, these trajectories reflect the 2024 federal cap on non-permanent residents — a structural break the older forecasts predate.

Under Regime B, the central reading is 9.2 million in 2055, rising to a central 12.5 million by 2080 within an 8.9–18.3 million envelope. ALTO’s 24-million target sits above the top of the 2055 envelope entirely — not at its optimistic edge, but beyond it.

The 24M target is the outlier

Set against the independent literature, the pattern is unambiguous: every other forecast clusters near the CRI central case, and the 24-million target stands alone above all of them. The reason the CRI figure sits lower than the academic studies is not methodological pessimism — it is one correction the others have not made.

The immigration inflection

The 2024–25 federal cap on non-permanent residents broke the corridor’s demographic trajectory, lowering the central forecast relative to pre-2024 expectations. Only the CRI analysis incorporates the NPR cap.

Pre-cap demographics elsewhere

All the independent forecasts — including the 2025 McGill and C.D. Howe studies — rest on pre-2024 population assumptions. They model a population surge that federal policy has since foreclosed.

Structural travel decline

Hybrid work and AI-mediated meetings structurally reduce corridor business travel below the pre-2020 baseline — a head-wind absent from the older forecasts entirely.

In other words, the daylight between ALTO’s target and the independent consensus is not a disagreement about how good high-speed rail is. It is the difference between forecasts built on a demographic future that is no longer the official plan and a forecast built on the one that is.

The 24-million target fails three independent feasibility tests

Each note tests the target from a different direction. The target does not fail one of them narrowly — it fails all three, and each failure is sufficient on its own.

Modal-shift framework

Reaching 24M requires a modal share above the 40 per cent ceiling implied by the North-American-calibrated S-curves in Notes 1 and 2. Even ALTO’s heaviest-subsidy regime, with deeply discounted fares, plateaus near 11–12 million annual riders at the modal-shift ceiling.

Demographic baseline

The 2024 federal Immigration Levels Plan capped non-permanent residents, producing a structural break in corridor population growth. Pre-2024 forecasts assumed continued surge; post-2024 trajectories are materially lower. 15–25 per cent of the gap to ALTO is demographic alone.

Subsidy frontier

Pushing past Regime A toward 24M requires operating subsidy above $5 billion per year, with full federal cost approaching $7 billion per year under the proponent’s own $75B capex base case — outside any defensible operating-regime choice on the corridor.

Three tests, one number

Read together, the three tests converge from independent premises on the same conclusion. They are not three versions of one argument; they are three different constraints, each of which the target violates.

Limit:~40% share ceiling (NA-calibrated)

Reaches:~11–12M even at heaviest subsidy

vs 24M?Falls short by half

Limit:Post-2024 NPR cap; 0.5–1.6%/yr growth

Reaches:9.2M central; 3.7–17.2M envelope

vs 24M?Above the upper bound

Limit:Defensible operating regimes (A–C)

Reaches:24M needs >$5B/yr operating subsidy

vs 24M?Outside any defensible regime

The convergence is the point. A target that merely sat at the optimistic edge of one analysis could be defended as ambition. A target that exceeds the modal-shift ceiling, sits above the demographic envelope, and requires an indefensible operating subsidy is not ambitious — it is, on the evidence of all four notes, 2.6× above what the corridor can carry.

Three questions to ask

Where the next federal or proponent statement on ALTO ridership is concerned — whether in a business case, a consultation report, or a public communication — three questions follow directly from the notes.

- On modal share: What rail share of the rail+air and rail+car markets does the 24-million target assume on each city-pair, and is that share calibrated on North-American or European travel behaviour?

- On demographics: Does the ridership forecast incorporate the 2024 federal cap on non-permanent residents, or does it rest on pre-2024 population assumptions that the cap has since superseded?

- On subsidy: At the fare level required to reach the target, what is the projected annual operating subsidy — and how does it compare with the $5 billion-plus the subsidy frontier implies under the proponent’s own capex base case?

None of these questions presupposes opposition to passenger rail, which is a widely shared public good. Each asks only that the project reconcile its headline number with the same evidence base — modal-shift behaviour, the demographic baseline, and the operating economics — that every other forecast for the corridor is built on.

Two numbers, one of them public

As of May 2026, ALTO’s public ridership figure is 24 million annual passengers by 2055. The independent evidence base — modal-shift behaviour calibrated to North America, a demographic baseline corrected for the 2024 immigration cap, and an operating-subsidy frontier built from the proponent’s own cost figures — places the corridor’s central case at 9.2 million. The two numbers are not a matter of optimism versus caution. The lower one incorporates evidence the higher one omits, and only the higher one has been put to the public.