Acquiring the Neighbourhood

What ALTO says publicly about land acquisition — the 60-metre right-of-way — and what a federal procurement document, released under Access to Information, shows the project was designed to do around its stations.

A Protected A federal slide deck — Subject-Specific Meeting #4B on Housing, dated April 10, 2024 — was released under Access to Information (file A-2025-00223, interim package). It was prepared for the consortia then bidding to become the project’s Private Developer Partner, roughly a year before the public consultations.

The deck sets out a federal strategy to use the rail project as a vehicle for housing and Transit-Oriented Development around each of the proposed station locations. Its first pillar is to acquire station-area land and define a framework for its development. ALTO has made no public statement about land value capture or station-area land assembly, and frames acquisition publicly around the 60-metre right-of-way alone.

The public discussion of ALTO expropriation runs together three different things. The first — the linear taking of a 60-metre right-of-way — is well documented. The second — fiscal and regulatory value-capture tools such as levies, charges and tax-increment financing — requires taking no one’s home. The third — station-area land assembly, in which a public body acquires a development portfolio around a station — does involve acquisition, and can reach beyond the operational footprint toward station-area homes; it is the variant urban residents have reason to watch.

The released procurement deck shows that the third was designed into the project at the bidding stage. The honest qualification, drawn from the federal government’s own infrastructure bank, is that the financial payoff Canadian evidence supports for this kind of assembly is modest and market-dependent — which raises a value-for-money question, not only an expropriation one.

A procurement notice that asks for more than track

In February 2026, Transport Canada published a tender for Financial Advisory Services to the high-speed rail initiative (solicitation T8080-240075). Among the advisory categories it lists are two that belong to a specific vocabulary: “Land value capture and community benefits advisory services” and “Transit-oriented Development and community benefits advisory services.” Transport Canada was, in other words, procuring the capacity to do land value capture — even though ALTO itself has said nothing public about it.

Land value capture (LVC) is the principle that public investment — a new station — raises the value of nearby land, and that the public purse can reclaim part of that uplift to help pay for the investment that created it. It is a respectable idea with a long international history. The question this brief addresses is narrower and more practical: how likely is LVC to feature in ALTO, and what would it mean for expropriation for people who live near a prospective station in Ottawa, Toronto or Montreal?

Until recently, the honest answer was “likely as a financing rationale, but the public record confines acquisition to the right-of-way.” A document released under Access to Information now allows a sharper answer.

What the procurement deck shows

The deck released under file A-2025-00223 is a Protected A federal presentation, “Housing and Transit-Oriented Development (TOD) — High Frequency Rail (HFR) Project, Subject-Specific Meeting #4B,” dated April 10, 2024. Its audience was the consortia then bidding to become the Private Developer Partner (PDP). Its purpose, stated on its own opening slide, was to explore how the project “can serve as a catalyst for housing development” and to describe Canada’s vision for “leveraging Transit-Oriented Development” near railway hubs.

Three features of the deck bear directly on the expropriation question.

A four-pillar housing strategy

Pillar 1, “Land & Real Property,” is to “identify lands along the proposed Alignment for station hubs and define a framework for their usage.” Pillar 4 is to leverage funding programs to “increase housing supply near station hubs.”

An acquire-then-develop sequence

The Provisional Guidelines slide states it plainly: “Canada would acquire the lands needed for the project and would explore with the PDP opportunities to optimize the development of station hubs.”

A worked visual concept

The deck renders an aerial of an Ottawa station hub ringed by mid- and high-rise towers — labelled a VIA HFR/QMOT 2023 concept, “for information and conceptual illustration only.”

The construction of that middle sentence is the heart of the matter. Canada acquires; Canada and the PDP then develop. That public-acquisition-then-development sequence is the defining shape of the land-assembly variant of value capture — the Hong Kong “Rail + Property” family of models — not of a simple right-of-way taking. The federal housing department of the day (then Infrastructure Canada, INFC; now Housing, Infrastructure and Communities Canada, HICC) appears throughout as a named party, alongside VIA-HFR, Transport Canada and the PDP.

This matters because it changes what kind of claim the Initiative can responsibly make. It is no longer necessary to infer a development intent from a procurement notice. The intent was set out, in a federal deck, to the people bidding to build the railway, a year before the public was consulted.

What “land acquisition” actually covers

The single phrase “land acquisition” is doing the work of three quite different things. They differ in what they take, from whom, and at what scale. Distinguishing them is the whole of the analysis.

Acquisition is framed around a “final right-of-way” of about 60 metres in width; the corporation will seek negotiated agreements at market value before resorting to expropriation.

ALTO public statements, May 2026

A linear taking: a continuous strip of land for track. The CEO has estimated the Ottawa–Montreal segment alone would cross roughly 1,700 properties, including about 500 farms.

Bill C-15 sharpens the federal acquisition powers: first right of refusal on coveted properties, prohibition-of-work orders, the ability to skip negotiation and go straight to expropriation, with objections routed to the Minister of Transport rather than an independent hearing.

“Land value capture and community benefits advisory services”; “Transit-oriented Development and community benefits advisory services.”

Transport Canada tender T8080-240075, February 2026

Four of the five LVC classes catalogued by the Canada Infrastructure Bank are fiscal or regulatory: infrastructure levies, development charges, density bonuses, and tax increment financing.

None of these requires taking anyone’s home. A homeowner near a station can be subject to a levy or a higher assessment without being expropriated at all. Montreal’s REM, for example, uses a $10/sq ft development charge in a zone around its stations — a tax, not a taking.

“Canada would acquire the lands needed for the project and would explore with the PDP opportunities to optimize the development of station hubs.”

A-2025-00223, Provisional Guidelines slide (April 10, 2024)

The fifth CIB class: “Land Acquisition, Investment and Disposition” — the public body acquires a land portfolio, then sells, leases, or jointly develops it. The CIB names the Hong Kong MTR Rail + Property model as the archetype.

The McGill TRAM study’s explicit recommendation is to “empower Alto to lead development and value capture within 2 km around the stations.” Two kilometres around a station is not a platform footprint — it is a neighbourhood.

The Ottawa case

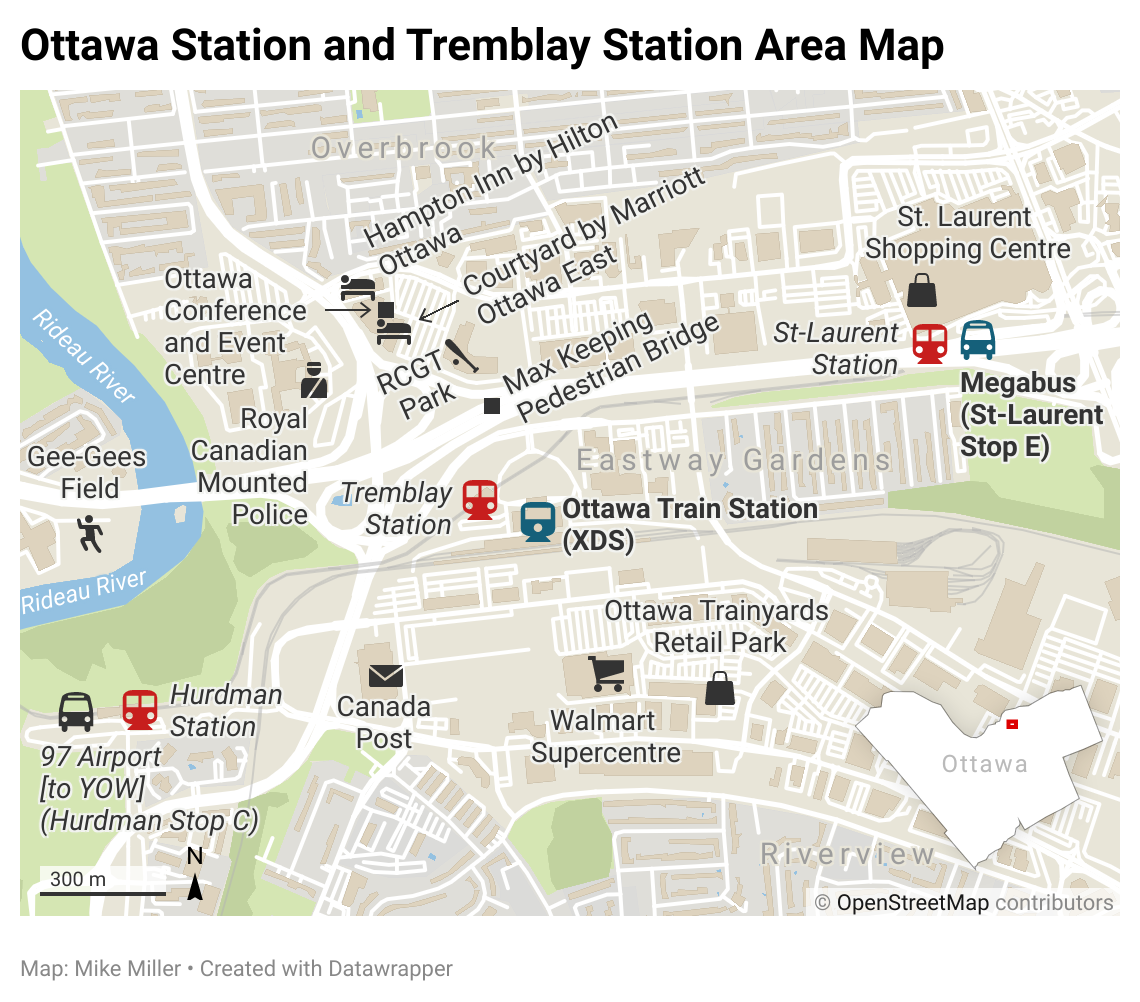

Eastway Gardens — the residential pocket east of the Tremblay Road stations, known locally as Ottawa’s “Alphabet Village” for its lettered avenues — is where the abstract distinction becomes concrete. Reporting in the Ottawa Citizen in May 2026 found a neighbourhood already living with the prospect: Alta Vista Councillor Marty Carr, who represents the area, said “the majority of residents in that neighbourhood think that it’s likely that a station would come there,” and described “a lot of trepidation, and a lot of unknowns,” with homeowners “very worried about expropriation.” Alto has identified the area as a potential Ottawa stop, and Carr believes “the space exists” on an empty parcel along Tremblay Road between Avenue U and St. Laurent Boulevard.

What makes that site attractive is the most telling detail in the reporting. Rideau-Vanier Councillor Stéphanie Plante — whose ward contains the downtown alternative, the former Union Station now serving as the Senate building — recounted what Alto had explained to her about the Tremblay option: “they have the space, it can be developed, the lands are ready to go.” David Jeanes of Transport Action Canada, who attended an Alto roundtable, noted the Tremblay area’s “significant intensification potential.” These are land value capture arguments in everything but name — and, in Plante’s account, they are Alto’s own framing of why Tremblay is preferred. The McGill study’s logic — prioritise “nodes with strong redevelopment and value-appreciation prospects rather than built-out downtown cores” — is exactly that reasoning, and it runs the same direction: toward the developable, ready site and away from the constrained downtown one. Alto’s CEO has said an above-ground station at the Senate building would “completely destroy the neighbourhood”; the Transport Minister cited the 2016 Rideau Street sinkhole and “geotechnical challenges” against it while praising the existing Tremblay station.

The expropriation question is, in the same reporting, explicitly an urban one and not only a rural one. The CEO estimated to Radio-Canada that the roughly 200 km of track between Ottawa and Montreal would cross about 1,700 properties, including some 500 farms — the linear taking. But residents along Avenue U voiced the wider worry directly, one noting the “really nice big space” between Avenue U and St. Laurent that a station might consume. The conceptual aerial in the released deck is, pointedly, an Ottawa station hub ringed by towers. A site chosen partly for its redevelopment headroom is the site where the gap between a right-of-way taking and station-area assembly is most likely to be tested. The Eastway Gardens trepidation is, on this evidence, responding to something real in the project’s own design documents — even as the public-facing messaging confines itself to the 60-metre strip.

What the federal evidence says the payoff is

The case for watching station-area assembly does not rest on assuming it will be lucrative. The opposite is closer to the truth, and it is the federal government’s own infrastructure bank that says so. The 2023 Canada Infrastructure Bank land value capture study — authored at the University of Toronto’s Infrastructure Institute — is sober about how much development-based LVC actually raises in Canada.

Modest sums, in practice

The study’s author characterises the record this way: rail-project value capture typically generates “tens of millions to hundreds of millions of dollars,” with only schemes catalysing large amounts of high-density development in high-value locations generating over a billion. Against an ALTO capital cost of $60–90 billion, the typical case is a rounding error per site; the billion-dollar case depends on exactly the intensification a site like Tremblay is being chosen for.

Hong Kong does not transplant

The Rail + Property model depends on Hong Kong’s state leasehold land tenure. The CIB is explicit that Canadian station areas have “fragmented ownership involving multiple public and private entities,” which makes the land assembly that powers the model difficult to convene.

This cuts two ways, and the Initiative should present both. It tempers the alarm: the financial incentive for aggressive, wholesale neighbourhood acquisition is weaker in the Canadian context than the McGill 15%-of-capital scenario implies, because the revenue simply has not materialised at that scale here. But it also sharpens a different concern. If the development-revenue payoff is modest and market-dependent, then the expropriation footprint of station-area assembly may be incurred for a fiscal benefit that does not arrive. That is a value-for-money question — the same family of question the Initiative’s subsidy-frontier work raises elsewhere — and it is at least as important as the expropriation question itself.

The McGill financial model illustrates the tension. Its self-sufficiency scenario depends on LVC contributing the equivalent of 15% of capital cost — on the order of C$12 billion against its C$79.8 billion construction estimate. The CIB’s evidence on realised Canadian deals suggests that figure is optimistic by a wide margin. The residents’ exposure, in other words, rests on a development-revenue premise that the more cautious Canadian evidence questions.

On this point the study’s author has spoken directly to the project. In a submission to the Senate Standing Committee on Transport and Communications, Matti Siemiatycki — who broadly supports value capture “as a matter of complementary public policy” — cautioned that the revenue-generating potential of LVC on the high-speed rail line is “likely limited by the few stations that Alto is proposing.” That is the author of the very study being applied to ALTO by name, reaching the same conclusion this section reasons toward: the development-revenue case is real but constrained, and the constraint is structural. (The caution is about how much LVC will recoup, not about expropriation; the inference that a constrained payoff weakens the case for an enlarged acquisition footprint is the Initiative’s.)

Three takings, one project

Read together, the three takings are not interchangeable. They differ in shape, in who is exposed, and in what the public record acknowledges.

Shape:Linear strip (~60 m)

Exposed:Corridor owners; ~1,700 properties Ott–Mtl

Public?Acknowledged

Shape:Levies, charges, TIF

Exposed:New development; no homes taken

Public?In tender only

Shape:Beyond the footprint (McGill: up to 2 km)

Exposed:Development land around the station

Public?In 2024 deck; not acknowledged publicly

The pattern is the disclosure asymmetry. The linear taking is discussed openly. The fiscal tools appear only in a procurement notice. The station-area assembly — the acquisition of development land beyond the line itself — was set out to bidders in 2024 and has not been part of any public ALTO communication since. That gap, now documented rather than inferred, is the brief’s subject.

How likely is land value capture — and what would it mean?

As with the cost and ridership questions, the answer depends on what is being asked.

Is LVC likely to feature in ALTO? On the evidence, yes — as a design intent. It is resourced in the tender, named in the federal housing mandate, modelled by McGill, and set out to bidders in the 2024 deck. What is not established is that it has survived into the Co-Development Phase as an executed land-assembly program. The deck is a procurement-stage document in the conditional voice — “would acquire,” “to be refined” — describing intent and a negotiating posture, not a finalised plan.

What would it mean for expropriation? That depends entirely on which of the three takings is meant. If ALTO’s value capture takes the fiscal form — levies and charges — the effect on station-area residents is financial, not displacement. If it takes the station-assembly form the 2024 deck describes, the effect can reach beyond the line into development land around the station — how far being the unanswered question — and the C-15 powers apply to that land as “needed for the project.” The deck shows the second was designed in; it does not show it has been executed.

The defensible position is therefore precise. The most alarming claim — “LVC means ALTO will expropriate your neighbourhood” — is not supported, and the CIB’s own evidence on modest Canadian returns argues against wholesale assembly being worth the trouble. But the reassuring claim — “acquisition is only the 60-metre right-of-way” — is contradicted by the federal government’s own procurement deck. The truth sits between the public messaging and the public fear, and the released document is what lets the Initiative locate it.

Three questions to ask

Where the next federal statement on ALTO land is concerned — whether in a corporate plan, a consultation report, or a public communication from ALTO — three questions follow.

- On scope of acquisition: Does “land needed for the project” mean the operational right-of-way only, or does it include development land for station hubs? If the latter, what is the geographic extent around each station, and on what basis is that land “needed”?

- On mechanism: Which form of value capture is contemplated — fiscal tools (levies, charges, TIF) that take no homes, or land assembly that does? If assembly, what is the expected development revenue, against what acquisition cost and footprint?

- On the business case: Given the Canada Infrastructure Bank’s own finding that Canadian development-based LVC has typically raised tens to hundreds of millions per deal — only the largest schemes exceeding a billion — what justifies the McGill model’s assumption of LVC at 15% of a $60–90 billion capital cost, and what expropriation footprint is being incurred to chase it?

None of these questions presupposes opposition to housing near transit, which is a widely shared public good. Each asks only that the project state plainly what its own 2024 design documents already contemplate — so that residents near a prospective station can know whether they are reading about a tax, a strip, or a neighbourhood.

There is also a constructive remedy already on the record. In his Senate submission, Siemiatycki recommends that the Bill C-15 acquisition powers “should only be used as a last resort,” and that “the original landowners should be given first right of refusal to repurchase any expropriated land not used for the project.” That second safeguard is precisely calibrated to the concern this brief identifies: a right to repurchase land not used for the project only matters if the project might acquire more than it uses — the surplus-acquisition dynamic that station-area assembly creates. Adopting it would cost the project nothing it needs and would directly answer the station-area resident’s fear.

Two accounts, one of them public

As of May 2026, ALTO’s public account of land acquisition is the 60-metre right-of-way. The federal procurement record released under Access to Information shows that, a year before the public consultations, the project was being co-developed with bidders as a vehicle for housing and Transit-Oriented Development whose first pillar was to identify and acquire station-area land. The two accounts are not contradictory, but the second is materially larger than the first — and only the first has been put to the public.